Annual Reports

GoDaddy Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Annual Report on Form 10-K — FY2025 (year ended Dec 31, 2025)

The latest 10-K — the fullest account of what GoDaddy is, how its two segments earn money, the risks that bite and what drove the year. · Open the full document →

Item 1. Business — Overview — p. 7 · Read the full section →

Management's plain-English definition: a one-stop shop for 20.4M entrepreneurs, organized around Identity, Presence and Commerce.

Item 1 Business, p.7 — GoDaddy as a one-stop shop for 20.4M entrepreneurs across Identity, Presence and Commerce.

GoDaddy is a global leader serving a large market of entrepreneurs, developing and delivering easy-to-use solutions as a onestop shop provider, backed by proactive, informed and personalized guidance. We serve small businesses, individuals, organizations, developers, designers and domain investors. […] Our 20.4 million customers are passionate and determined to transform their ideas into something meaningful. […] We design our solutions and tools to help our customers across all aspects of their businesses and to assist them in growing across what we call the "Entrepreneur's Wheel." The Entrepreneur's Wheel represents our customers' needs within three main focus areas: Identity, Presence and Commerce.

p. 7 · Read in context →

Item 1. Business — Core Platform: Domains — p. 16 · Read the full section →

The franchise that anchors the Core segment (~62% of revenue): the world's #1 registrar, where nearly every customer begins.

Item 1 Business — Domains, p.17 — the moat: ~81M domains under management, ~21% of all domains worldwide, ~94% of customers buy a domain.

We are the global leader in domain name registration, with approximately 81 million domains under management as of December 31, 2025. Based on information reported in VeriSign's most recent Domain Name Industry Brief, this represented approximately 21% of the approximately 387 million domain names registered worldwide as of December 31, 2025. As of December 31, 2025, approximately 94% of our customers purchased a domain from us.

p. 17 · Read in context →

We face significant competition for our products, which we expect will continue to intensify, and we may not be able to maintain or improve our competitive position or market share. — p. 50 · Read the full section →

A broad, low-switching market where GoDaddy fights niche point-solutions and full-suite rivals across its product lines, amplified by AI.

Risk Factors, p.50 — competition spans registrars, hosts, site builders, commerce, payments and email; management expects it to intensify.

The market for our products and services is highly competitive, and we expect this competition to continue in the future as existing and new competitors introduce new solutions or enhance existing solutions. […] Our competitors include providers of domain registration services, web-hosting solutions, website creation and management solutions, e-commerce enablement providers, payment facilitation providers, cloud computing service and online security providers, alternative web presence and marketing solutions providers and providers of productivity tools such as business-class email.

p. 50 · Read in context →

The relevant domain name registry and ICANN impose a charge upon each registrar for the administration of each domain name registration. If these fees increase, it would have a significant impact upon our operating results. — p. 81 · Read the full section →

GoDaddy has no control over the VeriSign/ICANN fees embedded in every .com; wholesale price hikes must be passed to customers or absorbed.

Risk Factors, p.81 — registry fees (e.g., VeriSign's .com) can rise at GoDaddy's expense; 'we have no control over ICANN, VeriSign.'

Each registry typically imposes a fee in association with the registration of a domain name. […] In addition, VeriSign, which operates the .com and .net gTLDs under registry agreements with ICANN and, with respect to the .com gTLD, a Cooperative Agreement with the U.S. Department of Commerce, has previously been given the right to annually increase prices, subject to certain limitations, and has done so in recent years […] If fees continue to increase, costs to our customers could become higher, which could have an adverse impact on our results of operations. We have no control over ICANN, VeriSign or other domain name registries and cannot predict their future fee structures.

p. 81 · Read in context →

GoDaddy Payments' risk management efforts may not be effective, and we could be exposed to substantial losses and liability which could substantially harm our business. — p. 96 · Read the full section →

The commerce growth bet carries settlement risk: as payment facilitator, GoDaddy eats fraud losses on funds it settles and can't recover.

Risk Factors, p.96 — loss exposure scales with seller size as GoDaddy settles transactions it may be unable to recover.

GoDaddy Payments offers payment processing and other payments products and services to our customers. We have programs to vet and monitor these customers, their GoDaddy Payments' accounts, and the transactions we process for them as part of our risk management efforts, but such programs require continuous improvement and may not be effective in detecting and preventing fraud and illegitimate transactions. When GoDaddy Payments' payments services are used to process illegitimate transactions, and we settle those funds to customers and are unable to recover them, we suffer losses and liability. As a greater number of sellers, including customers with larger sale volumes, use GoDaddy Payments' services, our exposure to material losses from a single seller, or from a small number of sellers, will increase.

p. 96 · Read in context →

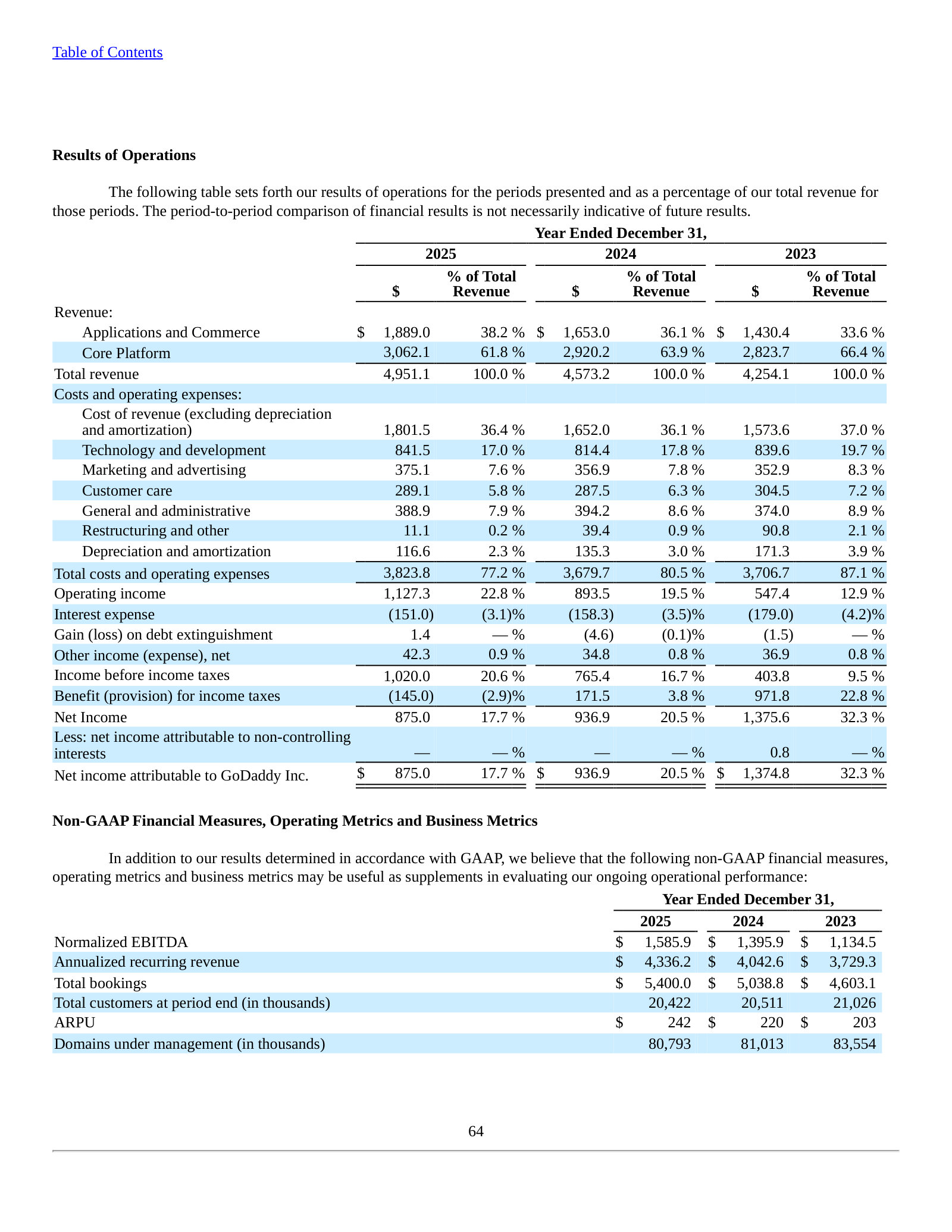

Item 7. Management's Discussion and Analysis — Overview — p. 113 · Read the full section →

Where management explains the model — a durable, recurring-subscription business with ~85% retention — and shows the FY2025 results.

MD&A Overview, p.114 — the recurring engine: ~85% retention five years, ~90% past three years, >89% of revenue from prior-year customers.

Strong customer retention continues to drive our business. We aim to attract high-intent customers that attach more at the outset of our relationship and over time. […] we know through our long history and vast amount of data that customers with a greater number of products with us retain at higher rates and produce higher lifetime value. In each of the five years ended December 31, 2025, our customer retention rate was approximately 85% […] In addition, the retention rate for our customers who had been with us for over three years as of December 31, 2025 was approximately 90%. Greater than 89% of our total revenue for the year ended December 31, 2025 was generated by customers who were also customers in the prior year.

p. 114 · Read in context →

Item 7. MD&A — Segment Results of Operations — p. 125 · Read the full section →

The segment split that matters: A&C (~38% of revenue) is the faster, higher-margin engine (+14% / 45% EBITDA) versus Core (+5% / 33%).

MD&A Segment Results, p.125 — the two segments GoDaddy manages by, measured on revenue and Segment EBITDA.

Our two operating segments, A&C and Core, reflect the way we manage and evaluate the performance of our business. Our chief operating decision maker evaluates segment performance based upon several factors, of which the primary financial measures are revenue and Segment EBITDA, our segment measure of profitability.

p. 125 · Read in context →

Item 7. Critical Accounting Policies and Estimates — Revenue Recognition — p. 130 · Read the full section →

The policy that defines the model: domain fees booked ratably over the term (deferred revenue), plus the principal-vs-agent gross/net test.

Annual Report on Form 10-K — FY2021 (year ended Dec 31, 2021)

Featured for one section — how management redefined a single segment of three product lines into today's two segments. · Open the full document →

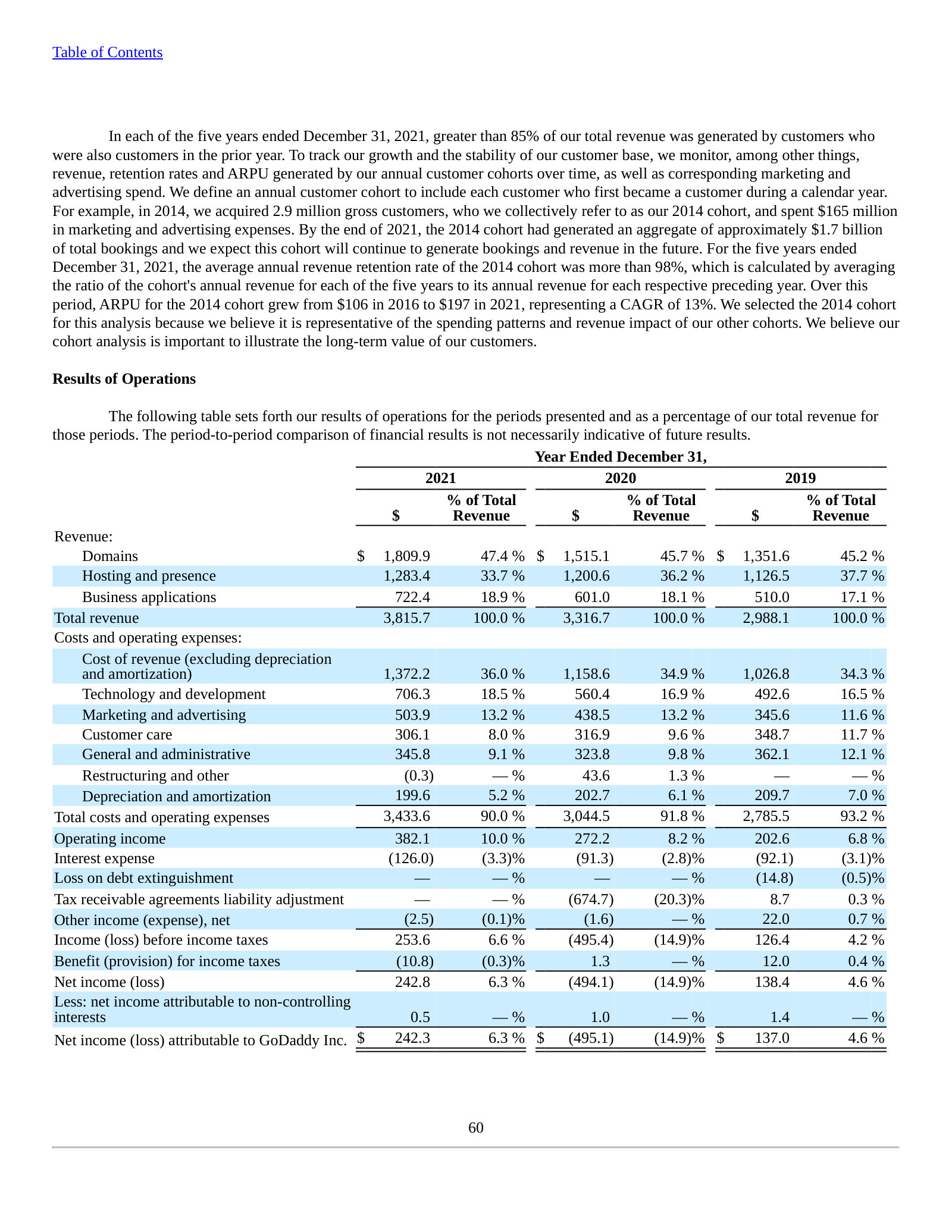

Item 7. MD&A — Results of Operations (revenue by product line) — p. 103 · Read the full section →

The pre-2022 view: one segment split into Domains, Hosting & presence and Business applications — before the A&C/Core redefinition.

More annual reports

Annual Report on Form 10-K — FY2024 (year ended Dec 31, 2024) · 197 pages · Prior-year 10-K; the immediate baseline for the FY2025 results and risk-factor comparison. · Open →

Annual Report on Form 10-K — FY2023 (year ended Dec 31, 2023) · 224 pages · FY2023 10-K, the first full year reporting under the A&C and Core two-segment structure. · Open →

Annual Report on Form 10-K — FY2022 (year ended Dec 31, 2022) · 211 pages · FY2022 10-K, the year GoDaddy transitioned to its Applications & Commerce and Core Platform segments. · Open →