Full Report

The numbers behind GoDaddy Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ millions unless noted.

Reading notes: Display units are US$ millions, per the filings' units line 'In millions, except shares in thousands and per share amounts'. Diluted share counts are shown in millions (filings print them in thousands). Each fiscal year is cited to that year's own Form 10-K primary column, except: (a) the FY2021 Applications and commerce / Core platform revenue split, which GoDaddy first reported under the current two-segment structure in the FY2022 10-K (the FY2021 10-K still used the legacy Domains / Hosting and presence / Business applications product lines), so FY2021's revenue-component citations point to the FY2022 10-K; and (b) FY2024 KPI figures, cited to the FY2025 10-K comparative column. Balance-sheet equity is the filings' bottom-line 'Total stockholders' equity (deficit)' (including non-controlling interests where present: FY2021 83.2 vs 81.7 attributable, FY2022 (329.3) vs (331.8), FY2023 62.2). FY2024-FY2025 had no non-controlling interests. The standardized data feed reports equity attributable to GoDaddy Inc.; the small differences are non-controlling interests, not restatements. Net income on the income statement is 'Net income attributable to GoDaddy Inc.'; net income on the cash-flow statement is total net income before non-controlling interests (e.g. FY2023 1,375.6 vs 1,374.8 attributable).

Share Price — Full Available History — 11 Years

The stock closed at $88.92 on Jul 10, 2026 — up 345% over the window shown (+14.1% a year), trading between $20.00 and $214.35. At that close the stock trades at 14× FY2025 diluted EPS as reported below.

Source: market price feed, weekly closes, sampled from 2,836 source observations, Mar 2015–Jul 2026. Price return only, excludes dividends.

FY2025 at a Glance

Revenue (US$ millions)

Operating income (US$ millions)

Net income (US$ millions)

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

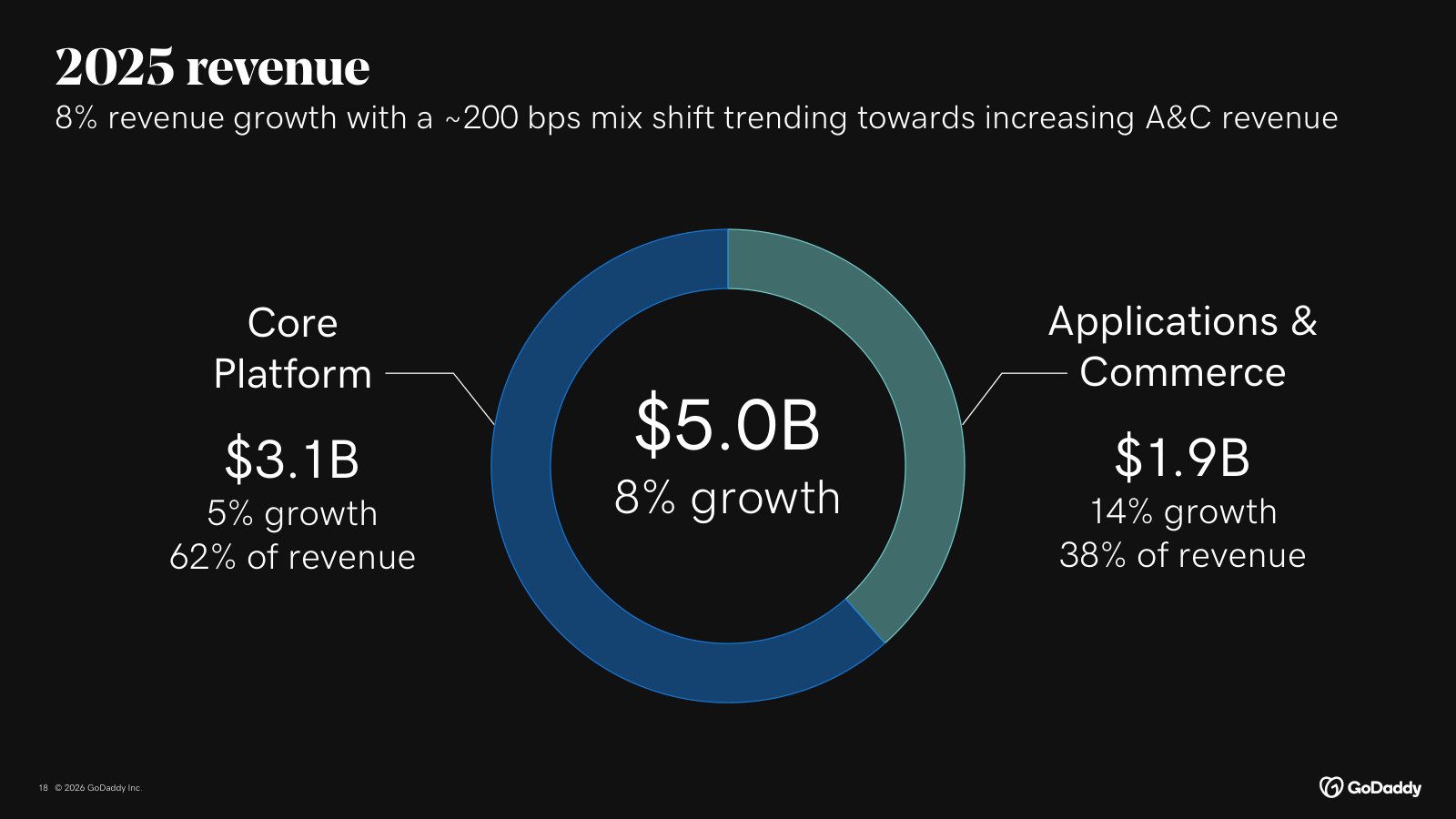

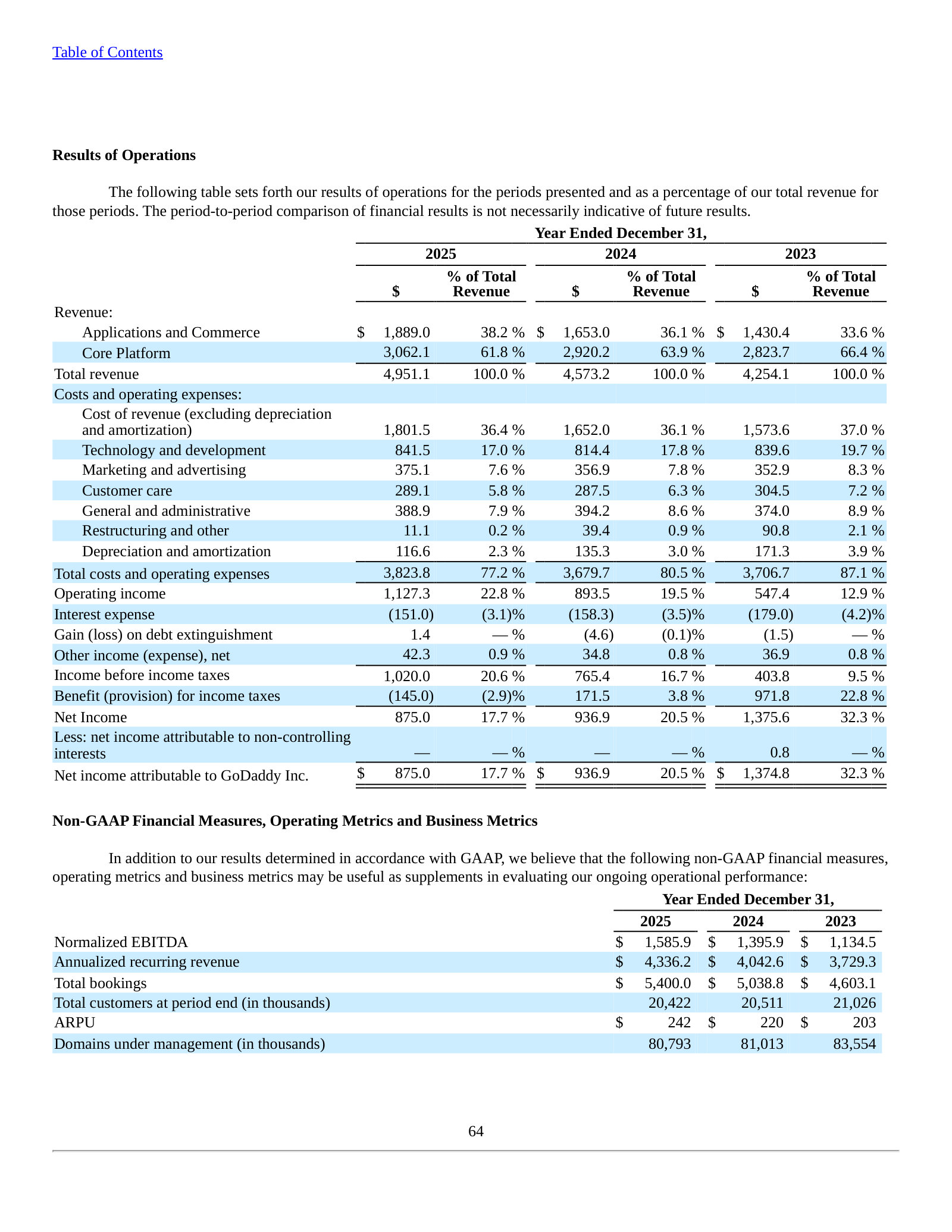

Revenue by Major Product Type

| Revenue by Major Product Type | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

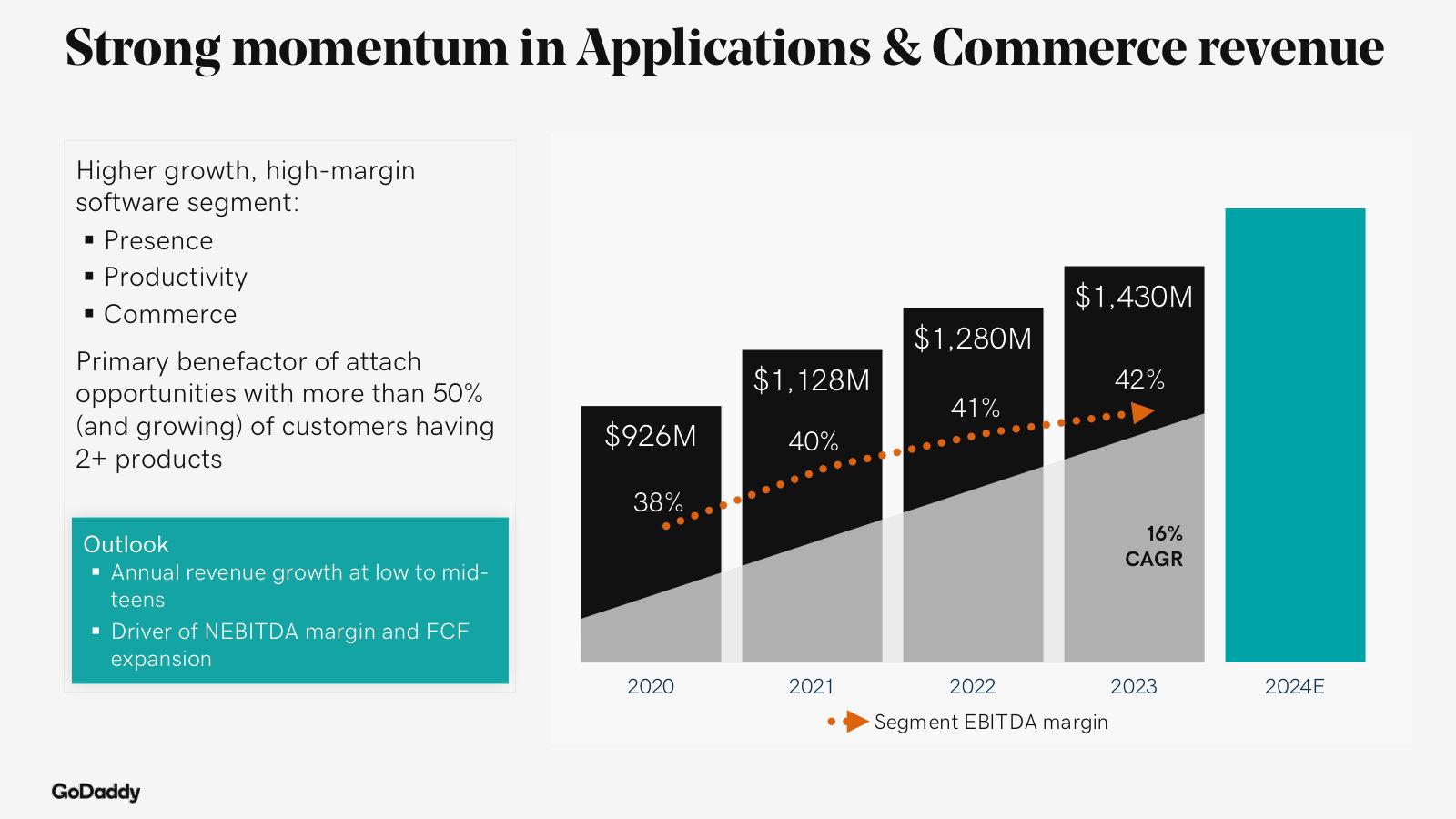

| Applications and commerce | 1,128 | 1,280 | 1,430 | 1,653 | 1,889 |

| Core platform: domains | 1,816 | 1,959 | 2,018 | 2,153 | 2,310 |

| Core platform: other | 872 | 852 | 805 | 768 | 752 |

| Total revenue | 3,816 | 4,091 | 4,254 | 4,573 | 4,951 |

| Total revenue growth, derived | — | +7.2% | +4.0% | +7.5% | +8.3% |

Source: Note 2 Disaggregated Revenue; Consolidated Statements of Operations [5] [1] [6] [2]. Click any linked figure to open the filing page with the row highlighted.

Segment EBITDA

| Segment EBITDA | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Applications and Commerce Segment EBITDA | 448 | 523 | 594 | 739 | 857 |

| Core Platform Segment EBITDA | 680 | 784 | 816 | 932 | 1,010 |

| Total Segment EBITDA | 1,127 | 1,306 | 1,411 | 1,671 | 1,867 |

Source: Note 17 Segment Information (Segment EBITDA) [7] [8] [9] [10]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Operations [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-13. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [11] [12] [13] [14]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [15] [16] [17] [18]. Click any linked figure to open the filing page with the row highlighted.

Revenue by Geography

| Revenue by Geography | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| U.S. | 2,545 | 2,757 | 2,873 | 3,113 | 3,324 |

| International | 1,271 | 1,334 | 1,381 | 1,460 | 1,627 |

| Total revenue | 3,816 | 4,091 | 4,254 | 4,573 | 4,951 |

Source: Note 2 Revenue by geography (customer billing address) [19] [1] [6] [2]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income attributable to GoDaddy Inc. | Diluted earnings per share | Net cash provided by operating activities |

|---|---|---|---|---|---|

| FY2016 | 1,848 | 50 | (16) | — | 386 |

| FY2017 | 2,232 | 67 | 136 | — | 476 |

| FY2018 | 2,660 | 150 | 77 | — | 560 |

| FY2019 | 2,988 | 203 | 137 | 0.76 | 723 |

| FY2020 | 3,317 | 272 | (495) | (2.94) | 765 |

| FY2021 | 3,816 | 382 | 242 | 1.42 | 829 |

| FY2022 | 4,091 | 499 | 352 | 2.19 | 980 |

| FY2023 | 4,254 | 547 | 1,375 | 9.08 | 1,048 |

| FY2024 | 4,573 | 894 | 937 | 6.45 | 1,288 |

| FY2025 | 4,951 | 1,127 | 875 | 6.22 | 1,599 |

Source: consolidated statements across filings; older years from the standardized feed [15] [1] [16] [2]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Total bookings | 4,232 | 4,414 | 4,603 | 5,039 | 5,400 |

| Annualized recurring revenue | 3,434 | 3,570 | 3,729 | 4,043 | 4,336 |

| Total customers at period end | 20,704,000 | 20,897,000 | 21,026,000 | 20,511,000 | 20,422,000 |

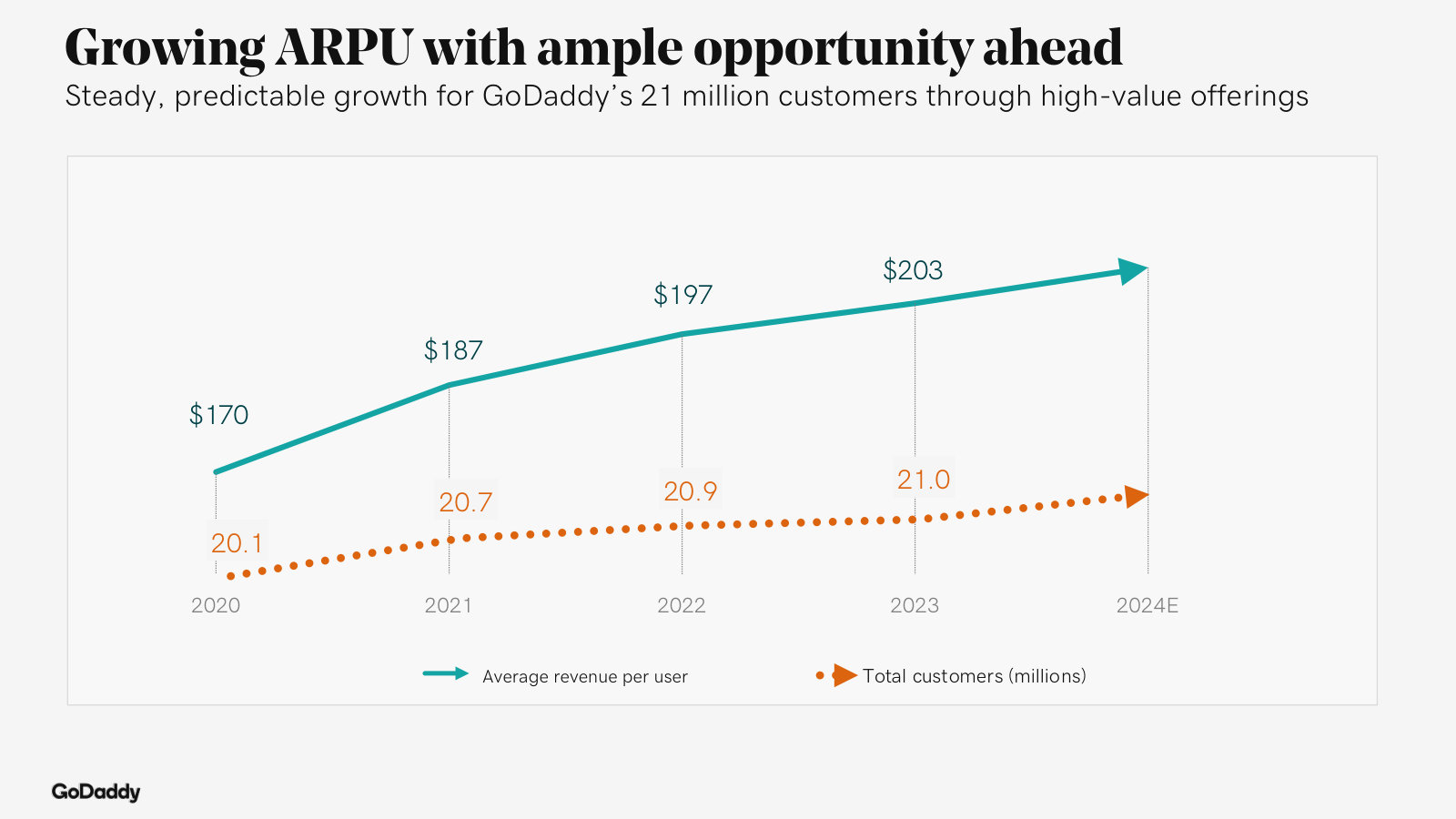

| Average revenue per user (US$) | 187 | 197 | 203 | 220 | 242 |

Source: company-reported operating metrics [20] [21] [22]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-13. Estimate figures link to the consensus source, not to filing pages.

Traceability

305 of 392 figures on this page (78%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

Display units are US$ millions, per the filings' units line 'In millions, except shares in thousands and per share amounts'. Diluted share counts are shown in millions (filings print them in thousands).

Each fiscal year is cited to that year's own Form 10-K primary column, except: (a) the FY2021 Applications and commerce / Core platform revenue split, which GoDaddy first reported under the current two-segment structure in the FY2022 10-K (the FY2021 10-K still used the legacy Domains / Hosting and presence / Business applications product lines), so FY2021's revenue-component citations point to the FY2022 10-K; and (b) FY2024 KPI figures, cited to the FY2025 10-K comparative column.

Balance-sheet equity is the filings' bottom-line 'Total stockholders' equity (deficit)' (including non-controlling interests where present: FY2021 83.2 vs 81.7 attributable, FY2022 (329.3) vs (331.8), FY2023 62.2). FY2024-FY2025 had no non-controlling interests. The standardized data feed reports equity attributable to GoDaddy Inc.; the small differences are non-controlling interests, not restatements.

Net income on the income statement is 'Net income attributable to GoDaddy Inc.'; net income on the cash-flow statement is total net income before non-controlling interests (e.g. FY2023 1,375.6 vs 1,374.8 attributable).

Total customers at period end for FY2021 is 20,704 thousand as reported in the FY2022 10-K; the FY2023 10-K shows a marginally restated 20,701 thousand for the same date. The difference is immaterial.

Quarterly cash-flow and balance-sheet statements are omitted: GoDaddy's 10-Qs print cash flows only on a year-to-date basis and the block here focuses on the single-quarter income statement, which the 10-Qs and the Q4 earnings 8-K print directly.

FY2016-FY2018 long-term figures are from the standardized data feed (SEC XBRL) and are shown without page links; FY2016-FY2018 diluted EPS is not available in the feed.

GoDaddy Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

2024 Investor Day — 2024

Management's fullest exposition of the business model, competitive advantages, segments, unit economics and the 2024–2026 financial framework. · Open the full document →

Q4 & Full-Year 2025 Earnings Results — Q4 / FY 2025

The current annual scorecard, plus management's fullest statement of the agentic-AI pivot made since the 2024 Investor Day. · Open the full document →

More from management

Q1 2026 Earnings Results — Q1 2026 · 36 pages · The latest quarter — most recent numbers, the refreshed investment thesis, and early Airo AI Builder traction ($10M+ run rate). · Open →

Q3 2025 Earnings Results — Q3 2025 · 38 pages · Where the 'Agentic Open Internet,' the .ai launch and the Agent Name Service were first laid out in detail. · Open →

GoDaddy Inc.'s management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

GoDaddy Q1 2026 Earnings Call — Q1 FY2026

Most recent call: how high-intent customers drive attach/ARPU, A&C vs Core economics, buyback-led capital allocation, and early Airo AI Builder traction. · Open the full transcript →

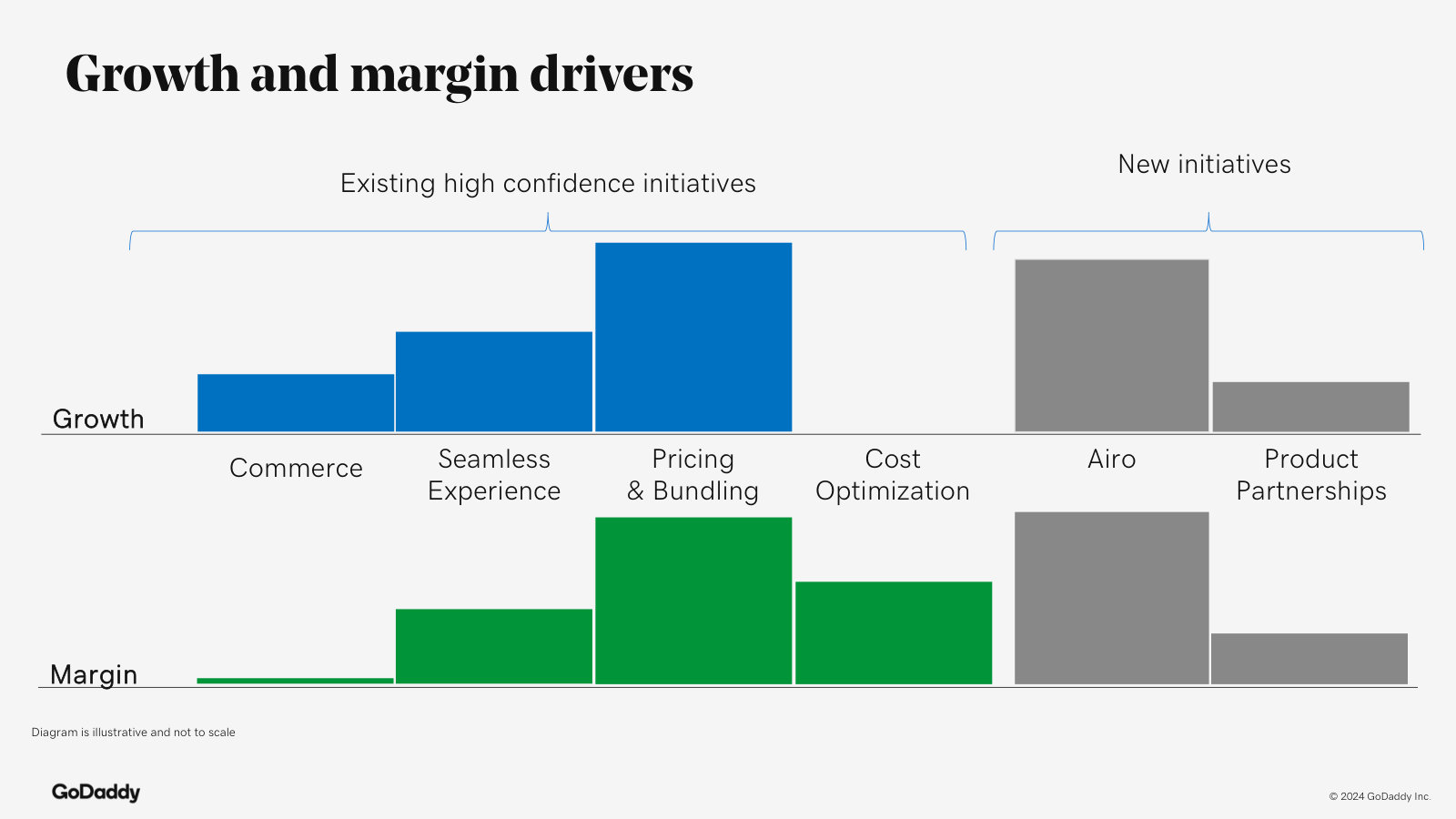

Segment structure and unit economics: A&C vs Core Platform margins, ARR mix, and the Airo-driven lift in $500+ customers.

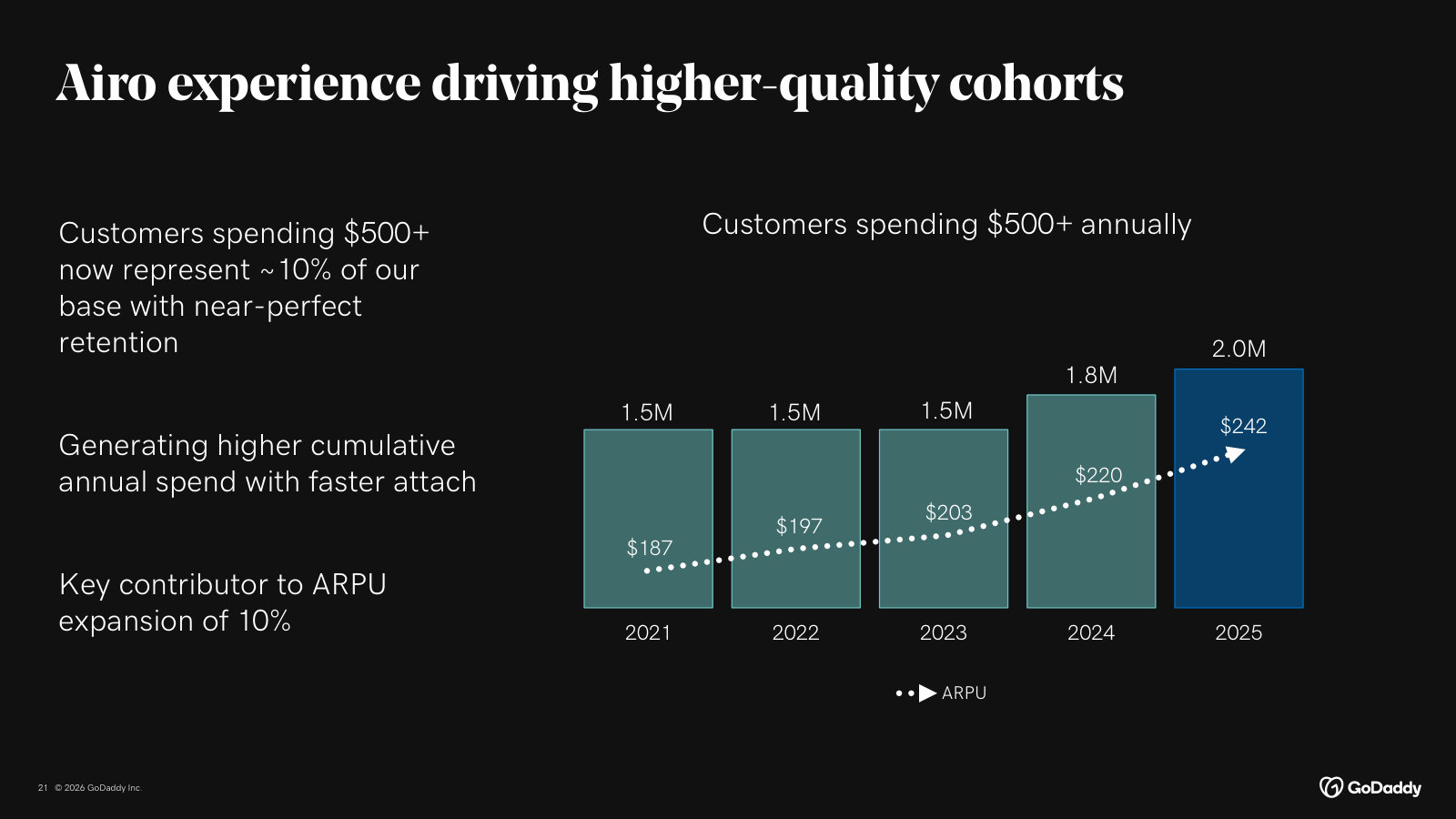

Mark McCaffrey, CFO: For our high-margin A&C segment, we drove 12% growth in revenue to $0.5 billion on continued solid attach of our subscription-based solutions. A&C ARR grew 10%, and this segment now represents approximately 40% of our total business. Segment EBITDA margin improved 110 basis points to 45% on product mix. Our Core Platform segment delivered revenue growth of 3% to $769 million, on 5% growth in primary domains with a stronger mix towards higher-priced non-.com TLDs. This was partially offset by softness in non-core GoDaddy hosting, the .CO registry contract expiration and tougher compares in aftermarket. Segment EBITDA margin expanded 150 basis points to 33% on product mix. […] And our newer Airo cohorts are demonstrating that higher value with second product attach accelerating 30% faster relative to non-Airo cohorts. These cohorts are contributing to the increase in the number of customers spending more than $500 annually, which represents approximately 10% of our customer base. Higher attach and retention rates above 85% drove ARPU growth of 9% to $246.

p. 3 · Read in context →

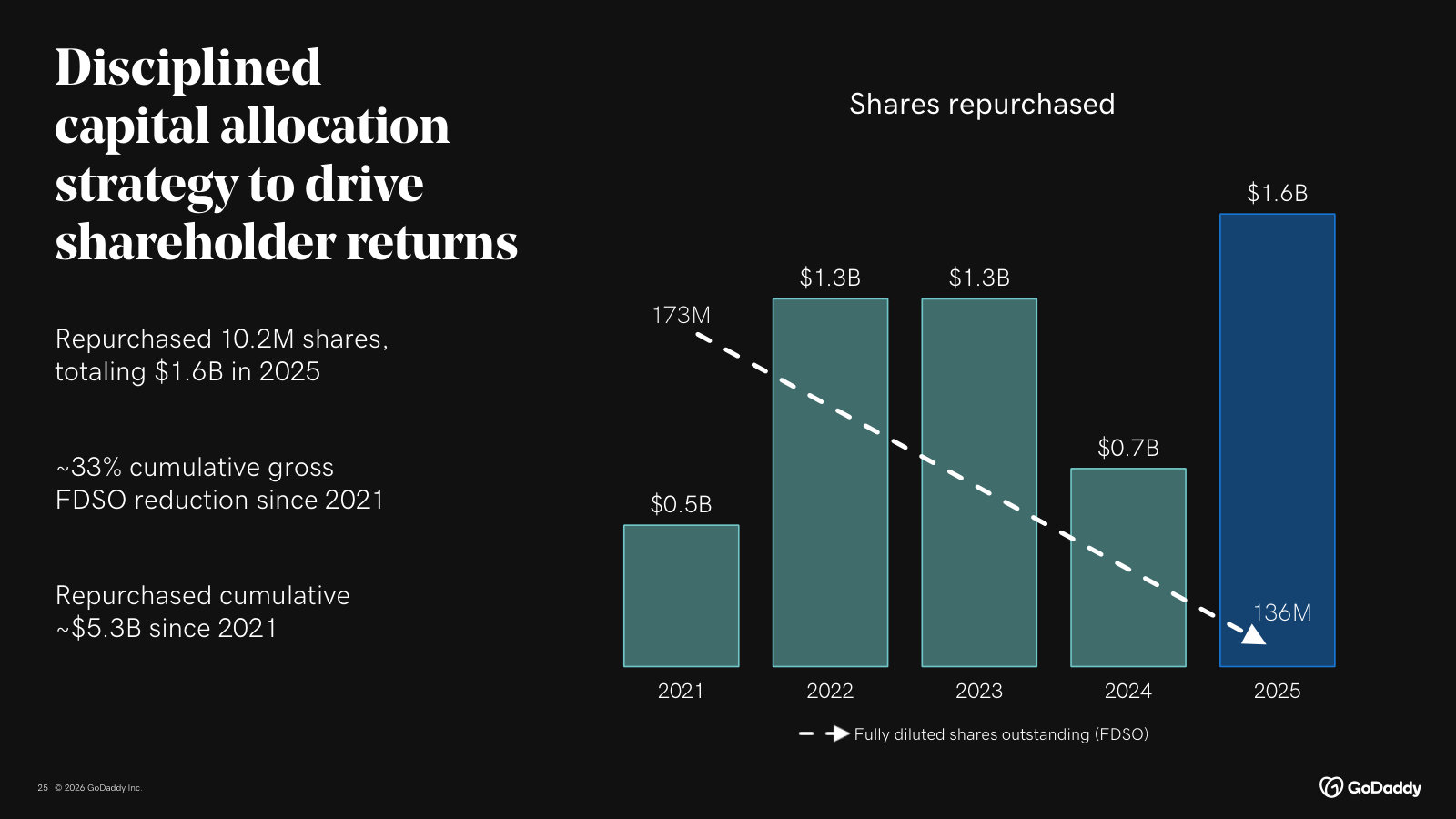

Capital-allocation and cash framework: over 95% of free cash flow to buybacks, above 1:1 EBITDA conversion, and a 20% free-cash-flow North Star.

Mark McCaffrey, CFO: Free cash flow grew 15% to $474 million, with a normalized EBITDA to free cash flow conversion of greater than 1:1. […] Since 2022, our share repurchase programs have resulted in a gross reduction in fully diluted shares outstanding of over 31%. And we ended the quarter with 133 million shares outstanding. […] For the full year, we expect normalized EBITDA to maintain a greater than 1:1 conversion to free cash flow, and we reaffirm our full year free cash flow target of approximately $1.8 billion. We continue to be on track to exceed our free cash flow North Star CAGR of 20%. On capital allocation. We operate within a disciplined, return-based framework and have deployed greater than 95% of our free cash flow over the last four years towards share repurchases.

p. 4 · Read in context →

How GoDaddy measures customer quality (high intent) and its philosophy for splitting AI efficiency gains between margin and reinvestment.

Vikram Kesavabhotla, Baird; Amanpal Bhutani, CEO; Mark McCaffrey, CFO: The way we define high intent is by looking at the traffic coming in by channel and then looking at the activation and attach of other products. And what we know from years and years of data across our 20 million customers is that if we see that activation and attach of other products, we are going to see good renewal at the end of the one-year term. […] we have the ability to expand our margins; we have for the past few years. We're continuing to see operational efficiencies by the adoption of AI internally. And then we're paying attention to the disciplined approach we've had in the past around investing in innovation, but using data points that show our path to return before we invest.

p. 5 · Read in context →

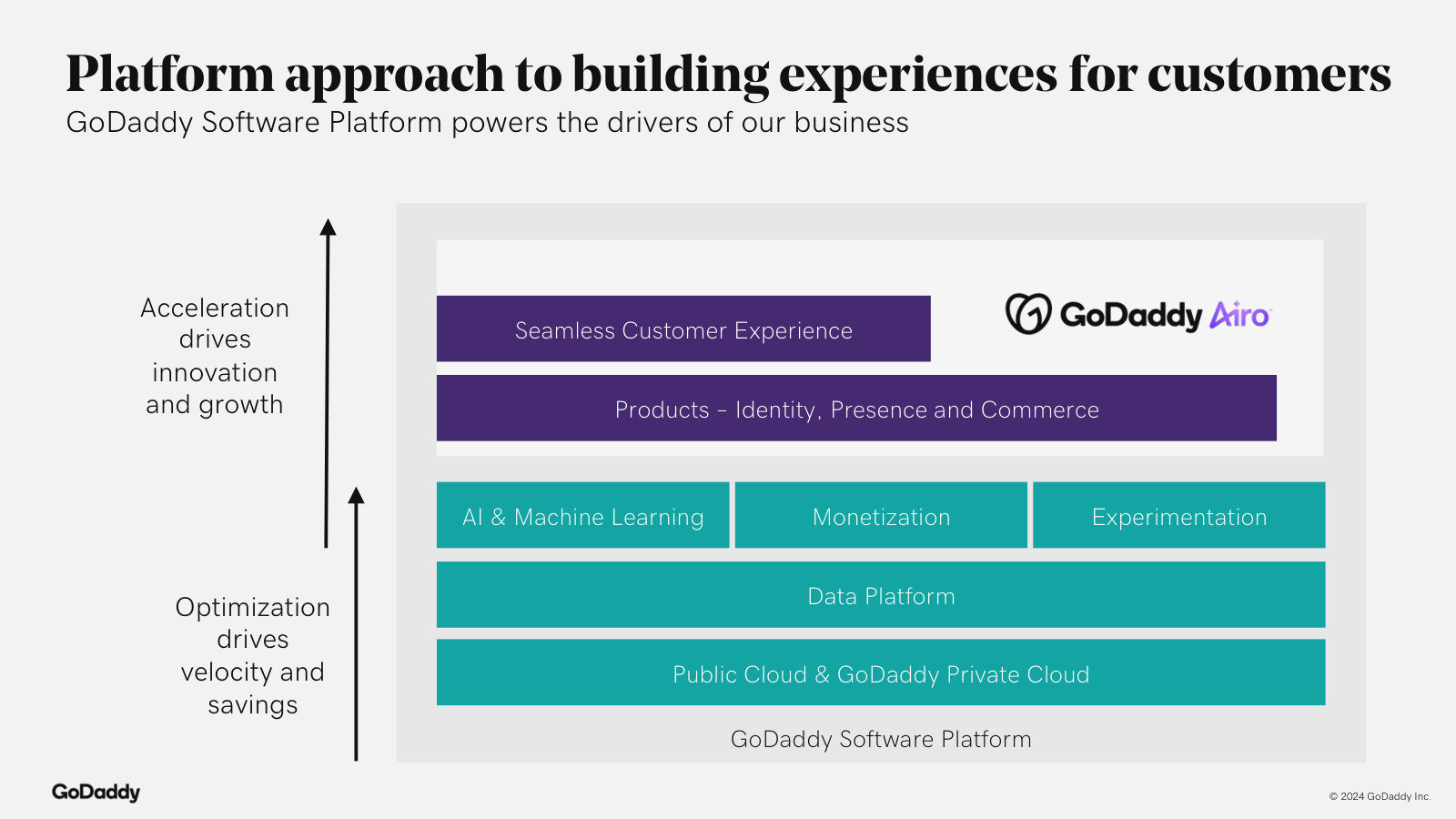

Airo AI Builder monetization mechanics — subscriptions plus credits, still-untapped domain/website funnels, and hosting as a differentiator.

Hoi-Fung (Ken) Wong, Oppenheimer; Amanpal Bhutani, CEO: When we talk about the $10 million run rate, we're really talking about annualized bookings. This is very early data. This includes both subscriptions and credits or tokens. We see customers come in by a subscription, engage with the product, enjoy the product, and they keep coming back […] We just started selling it in Care. We're going to add paid marketing starting this month. We also have the large funnels with domains and website paths which we haven't fully leveraged yet. […] Airo AI Builder does use GoDaddy hosting. It's one of our competitive differentiators. We can provide hosting at scale that's secure and cost-effective.

p. 6 · Read in context →

Hardest question: pressed for Airo unit economics — transaction size, credit-vs-subscription split, margin vs Websites + Marketing; management declines specifics.

Mark Zgutowicz, Benchmark; Amanpal Bhutani, CEO: You just closed $10 million in annualized bookings run rate for Airo AI Builder within weeks of beta. Could you break down the unit economics there? What's the average transaction size? How much of that run rate is coming from credit top-ups versus the initial plan purchase? And what's the margin profile relative to legacy Websites + Marketing? […] From day one, we've designed this product to be gross margin positive and to deliver appropriate economics. Regarding subscription versus credits, we're very early; this needs to bake and grow. […] It's too early to provide detailed disclosures on the split between subscription and credits.

p. 7 · Read in context →

Competitive positioning: a domain/DNS-based right to win in Agent Name Service, and willingness to let low-LTV domain customers go.

Eleanor Smith, JPMorgan; Amanpal Bhutani, CEO: GoDaddy has a strong right to win because within the ANS open standard we use the Domain Name System for discovery. DNS is a universal directory that replicates everywhere; agent registries are appearing across companies, and connecting those registries to the single DNS directory enables broad discovery. […] We have said we will let lower-LTV customers go because our focus is on high-intent customers. […] Our experience shows that value is in the high-intent customer: someone who buys a domain and then uses other products. That behavior drives LTV for GoDaddy and drives our business.

p. 9 · Read in context →

GoDaddy Q4 and Full Year 2025 Earnings Call — Q4 & FY2025

Annual call: the domains-to-attach LTV flywheel, the $500 cohort, AI cost discipline, and the 2026 .com go-to-market's bookings-vs-revenue trade-off. · Open the full transcript →

Segment economics and the funnel: A&C (47% margin) vs Core Platform, with domains as the front door and Airo driving attach.

Mark McCaffrey, CFO: For the Applications & Commerce segment, we drove 13% growth in revenue to $498 million on continued solid adoption and attach of our subscription-based solutions. Segment EBITDA margin improved 40 basis points to 47%. A&C ARR grew 12%. Our Core Platform segment delivered revenue growth of 3% to $776 million, driven by the continued strength in aftermarket, up 8% as well as 5% growth in primary domains, partially offset by the softness in non-core GoDaddy hosting. Segment EBITDA margin expanded 70 basis points to 35%. […] Domains remain the front door to our platform, attracting high-intent customers at a pivotal moment in their journey. Airo personalizes the experience that follows, accelerating discovery and increasing attach across identity, presence, and commerce.

p. 3 · Read in context →

The durable-growth engine: Airo LTV lift, the $500 cohort with near-perfect retention, ARPU flywheel, and 1,000 bps of five-year margin expansion.

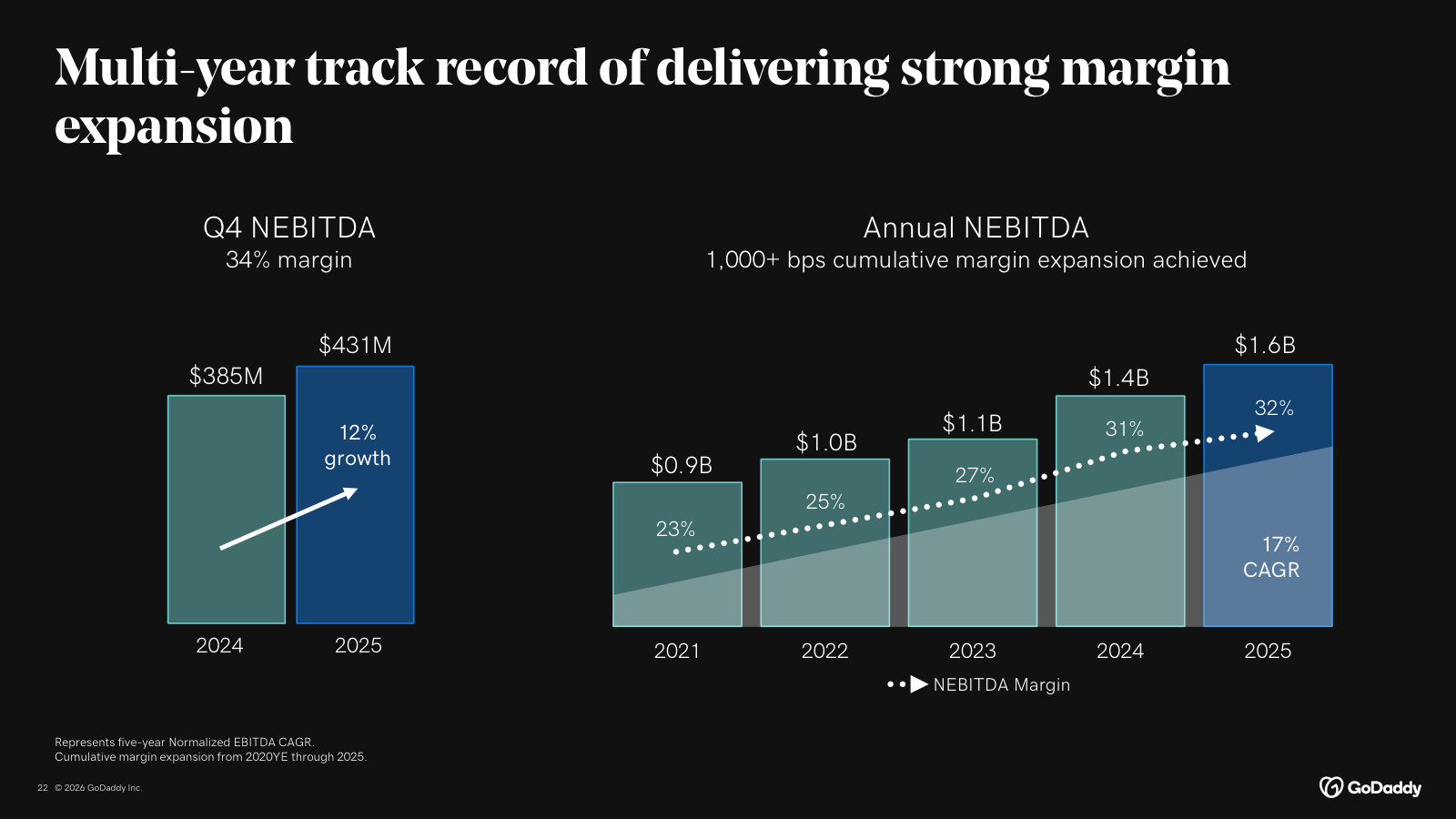

Mark McCaffrey, CFO: the velocity of a second product attach accelerated by nearly 30% relative to non-Airo cohorts. This dynamic is expanding lifetime value across our customer base. We see this most clearly in our highest value cohorts who spend more than $500 annually, which grew 11% and that represent approximately 10% of our total base. These customers have meaningfully higher second and third product attach rates and near-perfect retention. The result is compounding value creation with ARPU increasing 10% to $242 and overall retention rates rising above 85%. […] Over the past five years, cumulative margin expansion of 1,000 basis points reflects our ability to scale efficiently while continuing to invest in the business. This margin expansion flows through directly to cash generation. Free cash flow grew a robust 19% to $1.6 billion with a normalized EBITDA to free cash flow conversion of greater than 1:1.

p. 4 · Read in context →

Capital allocation and 2026 guidance: 100% of FCF to buybacks, ~33% cumulative share reduction, and the sizing of the 2026 revenue headwinds.

Mark McCaffrey, CFO: In 2025, we deployed 100% of our free cash flow, repurchasing 10.2 million shares totaling $1.6 billion while maintaining our balance sheet strength. Since 2021, our share repurchase programs have resulted in a gross reduction in fully diluted shares outstanding of approximately 33% and we ended the year with 136 million shares outstanding. […] With this, our full year revenue outlook incorporates just over 200 basis points of cumulative impact from the expiration of the .CO registry contract, the continued exclusion of high-value aftermarket transactions, and the go-to-market and product evolution we spoke about. The .CO and aftermarket impacts represent approximately two-thirds of this amount, while one-third is from the go-to-market and product evolution. […] We expect to drive free cash flow of approximately $1.8 billion, maintaining greater than a 1:1 conversion for the full year.

p. 4 · Read in context →

Hardest question, answered: whether the 2026 .com promo is a one-time or structural bookings drag, and why it barely touches revenue.

Mark McCaffrey, CFO (to Vikram Kesavabhotla, Baird): […] look at it from the multiyear terms to the annual terms. This is impacting our bookings, but has relatively little impact on revenue itself because the timing of the revenue recognition stays consistent. So that's one aspect of it. The other is there is a reduction in our average order size at initiation related to the discount that gets allocated amongst all the products, that does have a little bit of impact on revenue in and of itself. As time goes on, volume picks up, we get better at this offer. We think the major impact is going to be at the end of this year and going into Q1, but we expect that bookings to be in parity for the most part with revenue by the time we get to the end of the year.

p. 5 · Read in context →

AI cost economics: a single cost interface plus in-product cost optimization let GoDaddy fund more AI while holding its margin guidance.

Amanpal Bhutani, CEO: even as we look to invest in AI or the AI products, as we talked today, we have a couple of exciting product launches powered by AI, all of those sort of followed two core things. One, all the AI costs go through one interface so that we are able to stay on top of it very, very closely. It doesn't matter if that's a developer. It doesn't matter if it's one of the products that our customers are using. And two, we are very focused on solving for the objective function where we create products that are at a cost that works for our customers. So what you'll continually see in our products is an already optimized AI solution that then leads to lower costs than what you might see at some other companies. So those two things together, the visibility and the operational focus on it and the technological difference of just optimizing for that right within the product is what gives us confidence that we can continue to maintain the margin guidance that Mark has talked about while continuing to fund more and more use of AI, both within the company and with our products.

p. 6 · Read in context →

Competitive read on AI entrants: vibe-coding tools target enterprise/agency users, not GoDaddy's micro-business funnel — domains-plus-attach stays the moat.

Arjun Bhatia, William Blair; Amanpal Bhutani, CEO: When I look at the competitors in the AI space, we still continue to see a lot of that focus being on enterprise employees, like product managers, people that work within enterprises or people that are a little bit sort of working for agencies or companies like that. We see less of that behavior with our direct customer, the person who is the roofer, the cleaner, some micro business owner. So we see less of that. Our expansion of go-to-market is really about being able to bring more high-intent customers into the domains funnel, which is our largest funnel and then attach to it very well. […] I'm not suggesting that we are immune to what's happening in the world, we just have not seen a very large impact of that in our funnel yet or at this time.

p. 11 · Read in context →

GoDaddy Q4 and Full Year 2023 Earnings Call — Q4 & FY2023

The Airo launch call: first controlled-experiment monetization results, the A&C attach flywheel, and the FCF-per-share capital-return engine. · Open the full transcript →

Airo's first controlled experiment: the test cohort monetized above control via attach and mix shift to higher-price/margin products.

Aman Bhutani, CEO: On GoDaddy Airo, I have an update on its performance since launch. I am happy to share that in a controlled experiment, customers that were part of the first test cohort for the Airo experience monetized at rates higher than those customers in the control group that were not exposed to the Airo experience. The increased monetization was due to attach and shifting the mix towards higher price and higher margin products. This is particularly encouraging because significant customer experience changes like Airo typically take many months of iterative improvement to outperform the control group. With this initial promising result, we have rolled out GoDaddy Airo to more customers in the U.S. We have also launched tests in international markets a few days ago.

p. 2 · Read in context →

Segment unit economics: A&C is the high-margin engine — 13% revenue growth, 44% segment EBITDA margin, and GPV more than doubling to $1.7B.

Mark McCaffrey, CFO: Beginning with Q4 results, our high margin Applications and Commerce revenue grew 13% to $377 million and we delivered an expanded segment EBITDA margin of 44%, increasing 100 basis points since last quarter and 300 basis points since last year. ARR for Applications and Commerce grew 10% to $1.4 billion and our Create + Grow ARR was up 8% to $481 million. In Commerce, we drove significant growth in annualized GPV to $1.7 billion, more than doubling last year's performance as conversion of our existing customers to the GoDaddy software platform remains strong.

p. 2 · Read in context →

Capital-return engine plus the retention thesis: FCF/share +21%, over 20% share reduction ahead of schedule, and two-product customers giving pricing power.

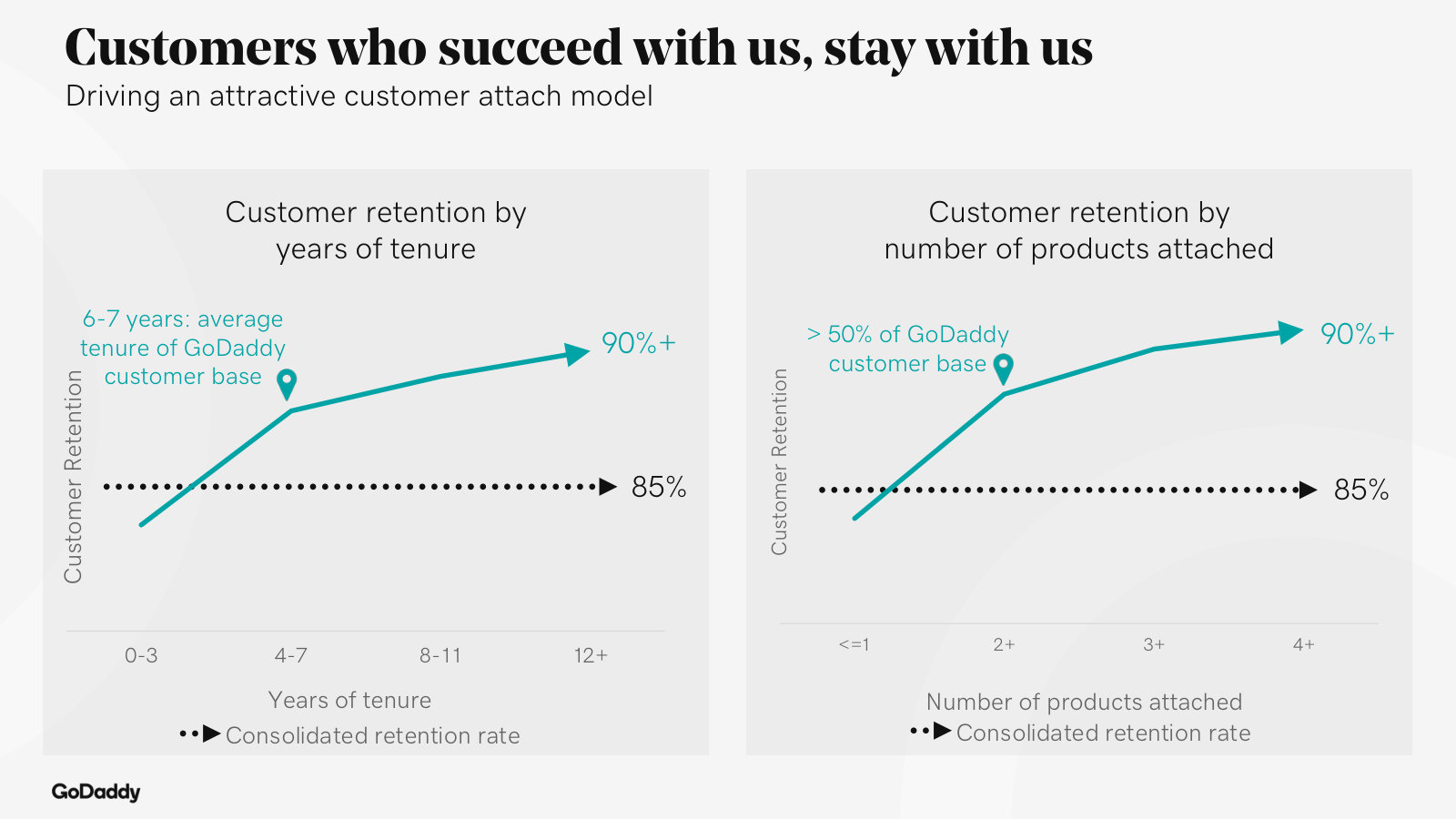

Mark McCaffrey, CFO: Additionally, the cumulative shares repurchased under our current authorizations totaled $2.6 billion, representing 34.2 million shares retired. This reduced our fully diluted shares outstanding since the inception of these authorizations by over 20%, achieving our three-year targeted reduction ahead of schedule. […] Customer retention remains 85% as we drove improvements in 2+ product attach, with greater than 50% of our customers paying for at least two products. These high-quality customers are stickier and give us greater pricing flexibility.

p. 3 · Read in context →

The attach flywheel quantified: second product → 85% retention, third product → 'almost a customer for life'; A&C bookings growing double digits across the board.

Mark McCaffrey, CFO; Aman Bhutani, CEO; Vikram Kesavabhotla, Baird: On A&C, the growth drivers, and we talk about this a lot, is we're seeing the demand move to that second product much faster than we had ever seen. And then now we're seeing it to the third product much faster than we've ever seen. So that shows up in our A&C growth. That's our higher profitability segment as well. […] We've talked about once we get to the second product, our average retention is 85%, but it goes up from there. If we get customers to a third product, it goes up significantly. It's almost a customer for life. So, those are the things that are driving the momentum in A&C right now

p. 7 · Read in context →

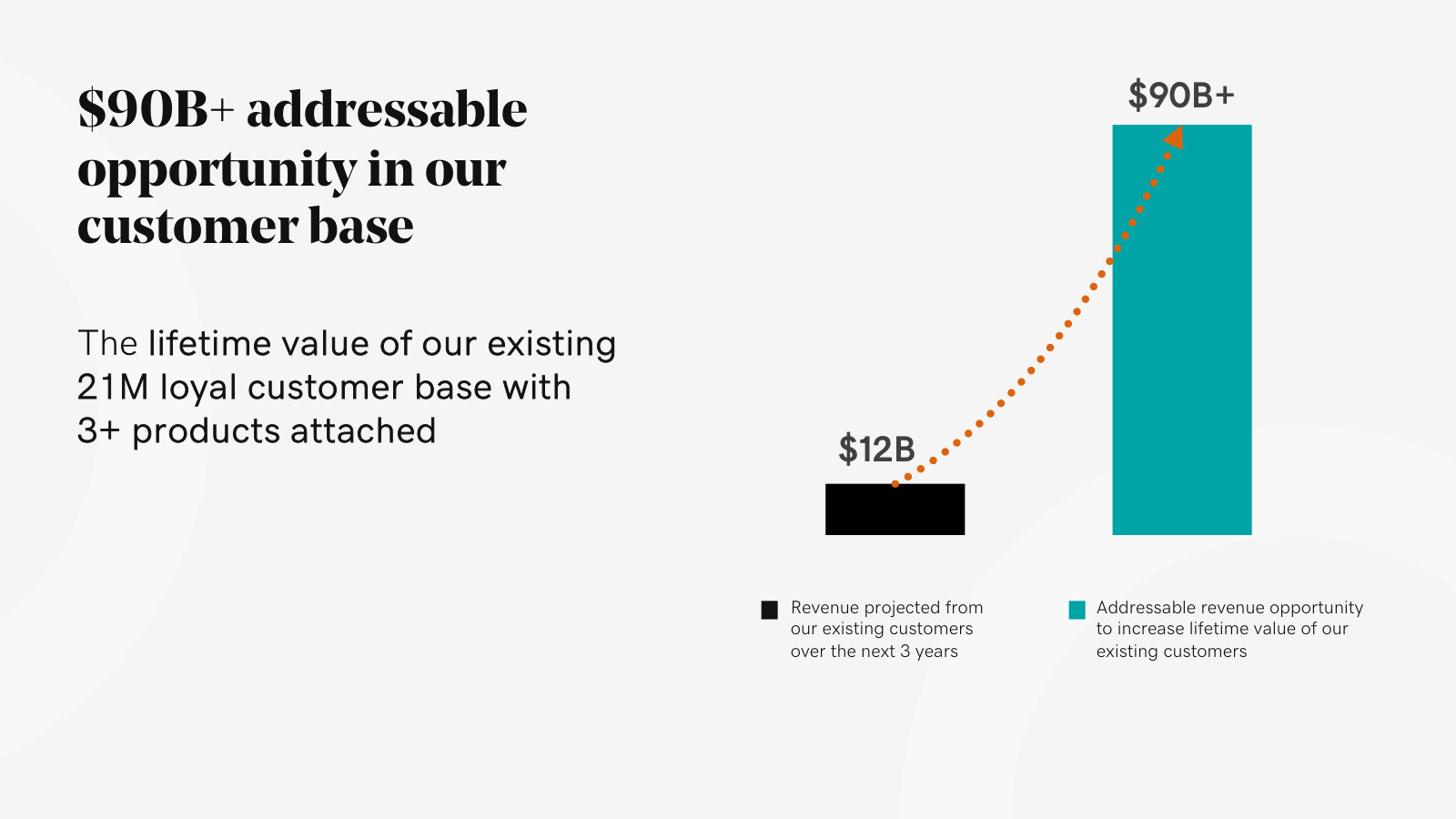

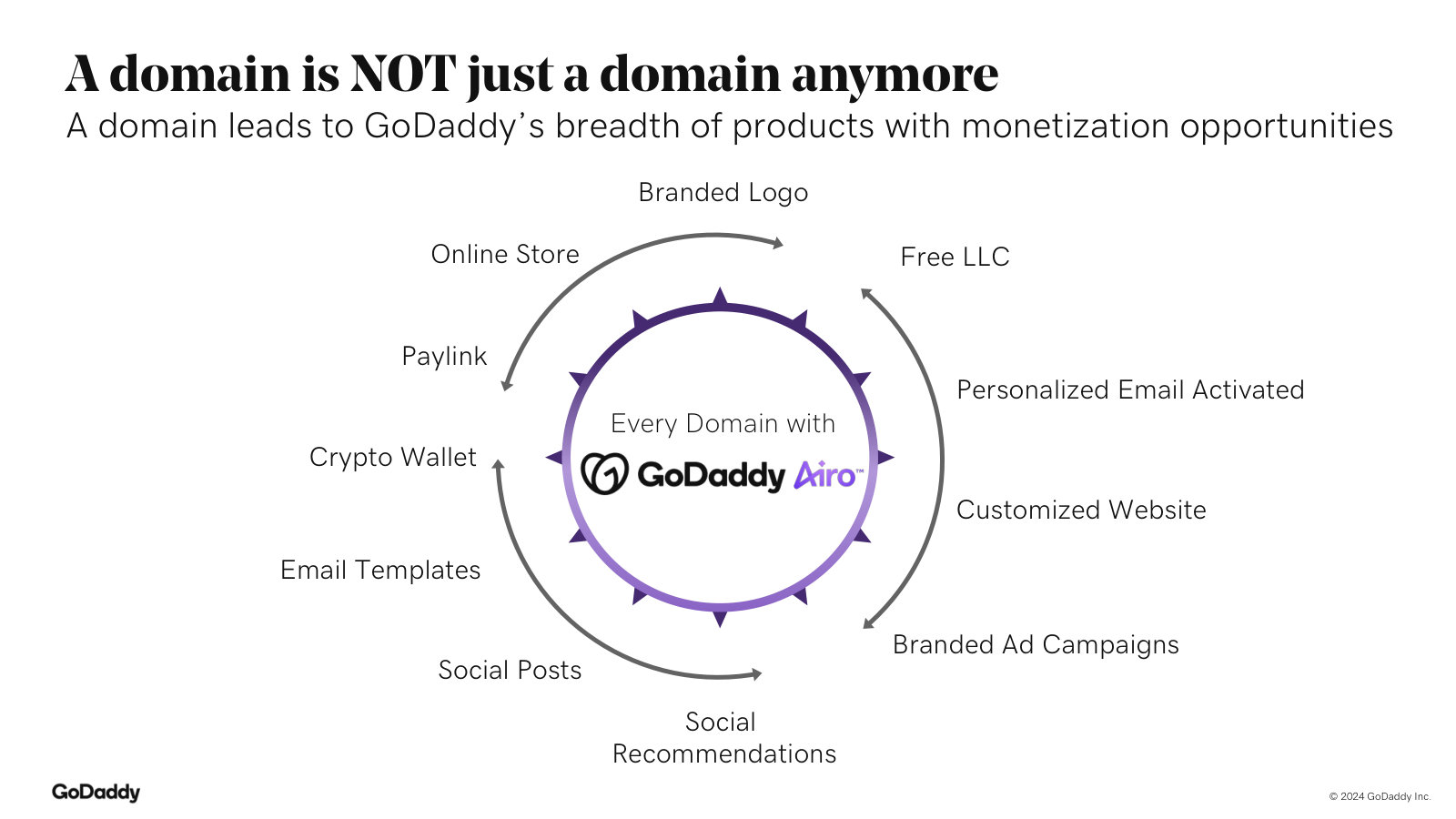

Airo monetization beyond attach: new paywalls GoDaddy has never run (e.g. premium logos), with 21M customers and 14M interactions feeding pricing.

Aman Bhutani, CEO; Evercore ISI: In terms of product attach and other monetization means, of course, product attach is the first level we're looking for. But as we'll share a little bit at our Investor Day, we're also looking for new monetization methods. And I'll just give you an example. One of the things that we want to test is a premium offering for logo building. […] And we're going to test a new paywall for it and a new monetization method that GoDaddy has never done before. […] And with 21 million customers, 14 million interactions with them, we get a lot of data about how they're getting value out of our products, which creates a lot of opportunity going forward around pricing bundles, elasticity around that, seeing the value they're driving.

p. 8 · Read in context →

Hardest question: why is net customer growth only ~1% vs 2-4% historically? A deliberate intent-based trade-off, shedding low-intent single-product customers.

Mark McCaffrey, CFO (to Ygal Arounian, Citigroup): When we look at our customers, we've always said we are targeting customers with a higher intent to do something when they come into the funnel, add that second product, start that business, generate value for themselves, and therefore generate value for us. What we've seen coming out of '23 and continuing into 2024 at the gross ads level is that consistent, strong demand that we've talked about all year and that continuing. And to put it in perspective, '23 gross customer ads was higher than 2022, right? And so not only are we seeing an increase there, we're seeing it more consistent from quarter to quarter and more stable. […] And we're seeing through the divestitures, we are losing customers, but they are generally customers that were low intent customers. So they were on a single product, maybe weren't doing things, hadn't done things for years. So that trade off is in there and continues to be something that we are working through on a net customer ad basis.

p. 9 · Read in context →

GoDaddy Q2 2022 Earnings Call — Q2 FY2022

Where the two-segment model (Applications & Commerce vs Core Platform) and the FCF-per-share buyback framework are laid out, plus the high-LTV pricing discipline. · Open the full transcript →

The Applications & Commerce segment defined: growth range, drivers, and ARR — the high-margin half of the two-segment model.

Mark McCaffrey, CFO: Applications and Commerce revenue grew 15% within the target range of 14% to 16%, driven by continued strength in our Create and Grow products and Email attach. The ARR for Applications and Commerce grew 12% to more than $1.2 billion. And within that, the ARR from our Create and Grow products grew 10% to $420 million.

p. 7 · Read in context →

Core Platform plus the capital-return math: unlevered FCF +16%, $1B of buybacks retiring ~8% of shares, FCF/share +19%, net leverage in range.

Mark McCaffrey, CFO: Unlevered free cash flow for the quarter totaled $274 million growing 16%, driven by strong profitability. Additionally, year to date, we completed $1 billion of share buybacks, repurchasing 12.8 million shares and reducing our fully diluted share count by approximately 8% since year-end. Free cash flow per share rose to $5.67 on a trailing 12-month basis versus the prioryear cash flow per share of $4.78, a 19% increase on strong cash flow and share repurchases. […] Net debt stands at $3.1 billion at the midpoint of our targeted range of two to four times.

p. 8 · Read in context →

How to read FX and pricing: currency hits bookings not costs, and price changes are tested nuanced by geography rather than rolled out globally.

Mark McCaffrey, CFO; Aman Bhutani, CEO; Trevor Young, Barclays: And then on pricing, yes, what you saw, Trevor, was us testing some changes, and those were the price test for Websites + Marketing. In terms of taking that international, as I've shared before, the price testing for us is quite nuanced. We base it on geography, on sort of customer expectations changing on market share. So you'll see it appear in certain geographies, but not in others. […] So most of the impact on the FX affects our bookings, our costs are pretty much fixed and in line with the U.S. dollar. So I would say, look for most of the FX impact to flow through to bookings and then ultimately lead to revenue with minimal impact on the cost in our structure today.

p. 11 · Read in context →

The retention thesis: products carrying large consumer surplus for high-LTV customers are the last spend they walk away from in a downturn.

Aman Bhutani, CEO (to Brent Thill, Jefferies): We add to that the fact that the products we sell create tremendous value for our customers and the price we charge, leaves plenty of consumer surplus for our customers, right? So even if they have to adapt to changing economic environment, the products we typically sell to them tend to be the last products they walk away from. So that's why we see sort of the continued high retention rates for customers.

p. 14 · Read in context →

How it makes money: bundling a payments-enabled checkout into the domain purchase itself - Commerce on every surface (the Omnicommerce ethos).

Aman Bhutani, CEO (to Mark Zgutowicz, Rosenblatt Securities): […] buy a domain, you get checkout page that you can customize that's enabled for your domain automatically. So you literally buy the domain and you can start taking payments, right? And that's a bit of a different movement in that we're not selling the product and then attaching more, we're bundling it in right with the first purchase and literally putting – and the idea there is put Commerce on every surface we have because that is, in a sense, the Omnicommerce ethos, right, like wherever you're transacting, whatever surface you're creating your commerce or your micro business is enabled in there.

p. 21 · Read in context →

Hardest question — is GoDaddy raising price on existing subs? Answer lays out the value-first pricing discipline that preserves consumer surplus.

Aman Bhutani, CEO; Naved Khan, Truist Securities: We have a large sort of broad portfolio of products. So we're constantly evaluating and doing tests and seeing where we should take price. And typically, we're taking price after we have added more value for the customer, right? We want to continue to push the willingness to pay up and then take price so that the surplus for the consumer continues to be maintained and the customer stay super happy with us.

p. 24 · Read in context →

More calls

GoDaddy Q4 and Full Year 2024 Earnings Call — Q4 & FY2024 · 16 pages · Airo's entry into the paid monetization phase (Airo and Airo Plus), the quality-over-quantity customer-base reset to 20.5M, and the 33%-margin-by-2026 path. · Open →

GoDaddy Q4 and Full Year 2021 Earnings Call — Q4 & FY2021 · 35 pages · The $3B (2022–2024) buyback authorization framed as ~80% of projected FCF, plus the ARPU/customer and transactional-aftermarket mechanics of the model. · Open →

GoDaddy Q3 2025 Earnings Call — Q3 FY2025 · 13 pages · For the most recent read before the 2026 go-to-market shift — Airo Builder ramp and momentum in the $500+ high-value cohort. · Open →

GoDaddy Q1 2024 Earnings Call — Q1 FY2024 · 13 pages · For the first full quarter after the Airo rollout and Investor Day, with early pricing-and-bundling execution against the durable-growth framework. · Open →

GoDaddy Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Annual Report on Form 10-K — FY2025 (year ended Dec 31, 2025)

The latest 10-K — the fullest account of what GoDaddy is, how its two segments earn money, the risks that bite and what drove the year. · Open the full document →

Item 1. Business — Overview — p. 7 · Read the full section →

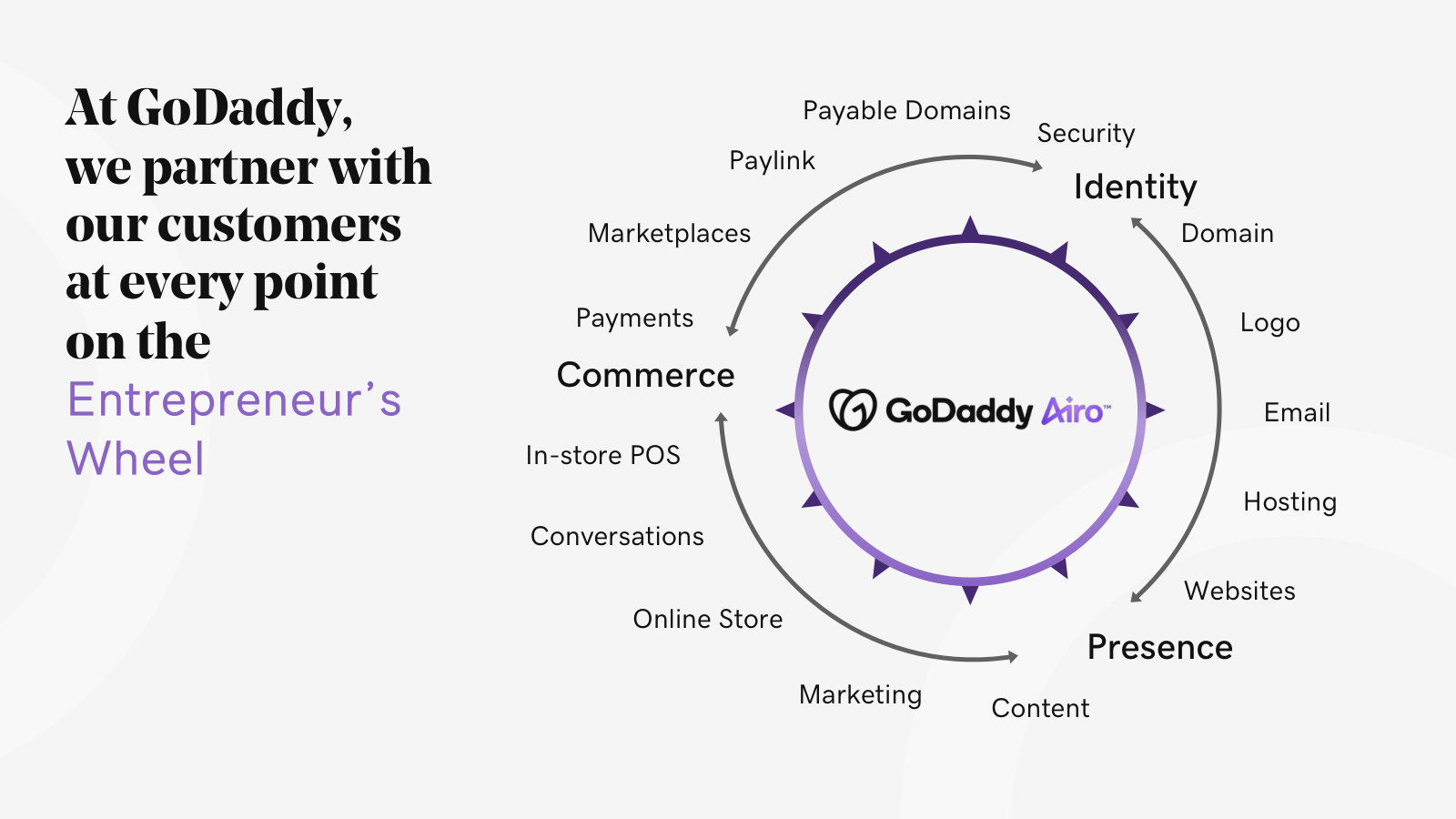

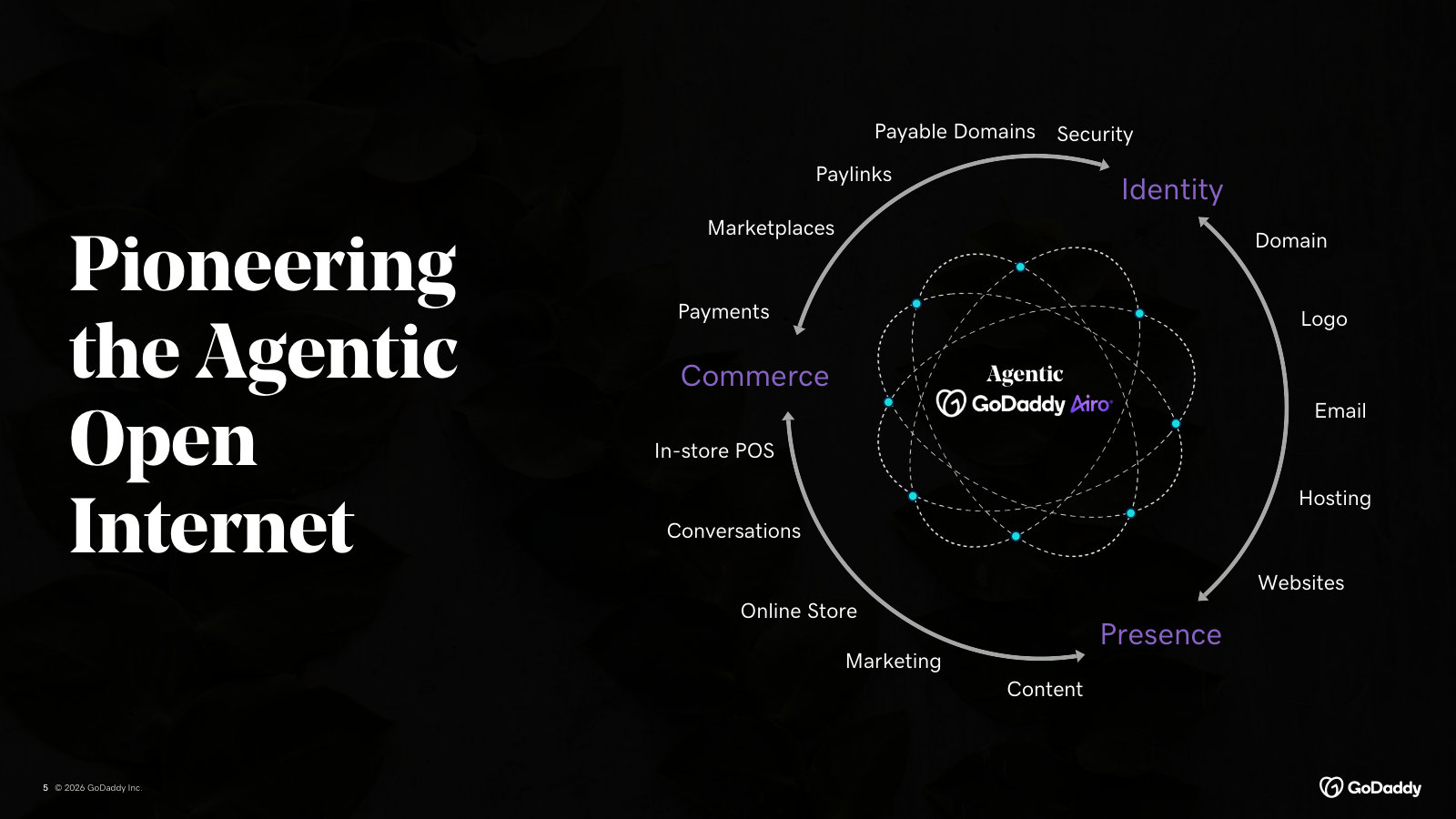

Management's plain-English definition: a one-stop shop for 20.4M entrepreneurs, organized around Identity, Presence and Commerce.

Item 1 Business, p.7 — GoDaddy as a one-stop shop for 20.4M entrepreneurs across Identity, Presence and Commerce.

GoDaddy is a global leader serving a large market of entrepreneurs, developing and delivering easy-to-use solutions as a onestop shop provider, backed by proactive, informed and personalized guidance. We serve small businesses, individuals, organizations, developers, designers and domain investors. […] Our 20.4 million customers are passionate and determined to transform their ideas into something meaningful. […] We design our solutions and tools to help our customers across all aspects of their businesses and to assist them in growing across what we call the "Entrepreneur's Wheel." The Entrepreneur's Wheel represents our customers' needs within three main focus areas: Identity, Presence and Commerce.

p. 7 · Read in context →

Item 1. Business — Core Platform: Domains — p. 16 · Read the full section →

The franchise that anchors the Core segment (~62% of revenue): the world's #1 registrar, where nearly every customer begins.

Item 1 Business — Domains, p.17 — the moat: ~81M domains under management, ~21% of all domains worldwide, ~94% of customers buy a domain.

We are the global leader in domain name registration, with approximately 81 million domains under management as of December 31, 2025. Based on information reported in VeriSign's most recent Domain Name Industry Brief, this represented approximately 21% of the approximately 387 million domain names registered worldwide as of December 31, 2025. As of December 31, 2025, approximately 94% of our customers purchased a domain from us.

p. 17 · Read in context →

We face significant competition for our products, which we expect will continue to intensify, and we may not be able to maintain or improve our competitive position or market share. — p. 50 · Read the full section →

A broad, low-switching market where GoDaddy fights niche point-solutions and full-suite rivals across its product lines, amplified by AI.

Risk Factors, p.50 — competition spans registrars, hosts, site builders, commerce, payments and email; management expects it to intensify.

The market for our products and services is highly competitive, and we expect this competition to continue in the future as existing and new competitors introduce new solutions or enhance existing solutions. […] Our competitors include providers of domain registration services, web-hosting solutions, website creation and management solutions, e-commerce enablement providers, payment facilitation providers, cloud computing service and online security providers, alternative web presence and marketing solutions providers and providers of productivity tools such as business-class email.

p. 50 · Read in context →

The relevant domain name registry and ICANN impose a charge upon each registrar for the administration of each domain name registration. If these fees increase, it would have a significant impact upon our operating results. — p. 81 · Read the full section →

GoDaddy has no control over the VeriSign/ICANN fees embedded in every .com; wholesale price hikes must be passed to customers or absorbed.

Risk Factors, p.81 — registry fees (e.g., VeriSign's .com) can rise at GoDaddy's expense; 'we have no control over ICANN, VeriSign.'

Each registry typically imposes a fee in association with the registration of a domain name. […] In addition, VeriSign, which operates the .com and .net gTLDs under registry agreements with ICANN and, with respect to the .com gTLD, a Cooperative Agreement with the U.S. Department of Commerce, has previously been given the right to annually increase prices, subject to certain limitations, and has done so in recent years […] If fees continue to increase, costs to our customers could become higher, which could have an adverse impact on our results of operations. We have no control over ICANN, VeriSign or other domain name registries and cannot predict their future fee structures.

p. 81 · Read in context →

GoDaddy Payments' risk management efforts may not be effective, and we could be exposed to substantial losses and liability which could substantially harm our business. — p. 96 · Read the full section →

The commerce growth bet carries settlement risk: as payment facilitator, GoDaddy eats fraud losses on funds it settles and can't recover.

Risk Factors, p.96 — loss exposure scales with seller size as GoDaddy settles transactions it may be unable to recover.

GoDaddy Payments offers payment processing and other payments products and services to our customers. We have programs to vet and monitor these customers, their GoDaddy Payments' accounts, and the transactions we process for them as part of our risk management efforts, but such programs require continuous improvement and may not be effective in detecting and preventing fraud and illegitimate transactions. When GoDaddy Payments' payments services are used to process illegitimate transactions, and we settle those funds to customers and are unable to recover them, we suffer losses and liability. As a greater number of sellers, including customers with larger sale volumes, use GoDaddy Payments' services, our exposure to material losses from a single seller, or from a small number of sellers, will increase.

p. 96 · Read in context →

Item 7. Management's Discussion and Analysis — Overview — p. 113 · Read the full section →

Where management explains the model — a durable, recurring-subscription business with ~85% retention — and shows the FY2025 results.

MD&A Overview, p.114 — the recurring engine: ~85% retention five years, ~90% past three years, >89% of revenue from prior-year customers.

Strong customer retention continues to drive our business. We aim to attract high-intent customers that attach more at the outset of our relationship and over time. […] we know through our long history and vast amount of data that customers with a greater number of products with us retain at higher rates and produce higher lifetime value. In each of the five years ended December 31, 2025, our customer retention rate was approximately 85% […] In addition, the retention rate for our customers who had been with us for over three years as of December 31, 2025 was approximately 90%. Greater than 89% of our total revenue for the year ended December 31, 2025 was generated by customers who were also customers in the prior year.

p. 114 · Read in context →

Item 7. MD&A — Segment Results of Operations — p. 125 · Read the full section →

The segment split that matters: A&C (~38% of revenue) is the faster, higher-margin engine (+14% / 45% EBITDA) versus Core (+5% / 33%).

MD&A Segment Results, p.125 — the two segments GoDaddy manages by, measured on revenue and Segment EBITDA.

Our two operating segments, A&C and Core, reflect the way we manage and evaluate the performance of our business. Our chief operating decision maker evaluates segment performance based upon several factors, of which the primary financial measures are revenue and Segment EBITDA, our segment measure of profitability.

p. 125 · Read in context →

Item 7. Critical Accounting Policies and Estimates — Revenue Recognition — p. 130 · Read the full section →

The policy that defines the model: domain fees booked ratably over the term (deferred revenue), plus the principal-vs-agent gross/net test.

Annual Report on Form 10-K — FY2021 (year ended Dec 31, 2021)

Featured for one section — how management redefined a single segment of three product lines into today's two segments. · Open the full document →

Item 7. MD&A — Results of Operations (revenue by product line) — p. 103 · Read the full section →

The pre-2022 view: one segment split into Domains, Hosting & presence and Business applications — before the A&C/Core redefinition.

More annual reports

Annual Report on Form 10-K — FY2024 (year ended Dec 31, 2024) · 197 pages · Prior-year 10-K; the immediate baseline for the FY2025 results and risk-factor comparison. · Open →

Annual Report on Form 10-K — FY2023 (year ended Dec 31, 2023) · 224 pages · FY2023 10-K, the first full year reporting under the A&C and Core two-segment structure. · Open →

Annual Report on Form 10-K — FY2022 (year ended Dec 31, 2022) · 211 pages · FY2022 10-K, the year GoDaddy transitioned to its Applications & Commerce and Core Platform segments. · Open →

Competitors describe GoDaddy Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Wix.com Ltd. (WIX)

Wix is GoDaddy's closest website-builder and online-presence rival for the same small-business and entrepreneur customer, and its 10-K names GoDaddy directly as a competitor in web creation.

Wix's 10-K competition section names GoDaddy directly — grouping it with large domain-registration and hosting companies whose website-building tools overlap Wix's own — and flags generative-AI website builders as an emerging overlap.

Additionally, several large service companies that primarily offer domain registration and hosting services, such as GoDaddy, provide the ability for a business owner to build a website using their tools or have one built by their workforce. Moreover, newly emerging technologies that utilize AI may also offer services that overlap with certain solutions we offer, including the emergence of generative AI website builders.

p. 106 · Read in context →

Wix's stated scale on the shared SMB web-presence market: roughly 282.4 million registered users who began building a website with it, and about 6.2 million paid premium subscriptions at year-end 2024.

As of December 31, 2024, we empower approximately 282.4 million registered users worldwide who began the website building process with us. […] as of December 31, 2024, we had approximately 6.2 million premium subscriptions.

p. 84 · Read in context →

Wix's account of its AI Website Builder, an AI-chat-driven site generator — the product category where it competes with GoDaddy's AI-assisted site creation.

These tools include our AI Website Builder, a pioneer website generator that creates a ready-to-publish website integrated with relevant business applications, from a short conversational AI chat with users

p. 85 · Read in context →

IONOS Group SE (IOS)

IONOS is essentially GoDaddy's European analog — a full-stack domains, web-hosting, website-building and cloud provider selling the same land-and-expand bundle to small and medium-sized businesses.

IONOS's stated view of the SMB digitalization funnel — starting at domain and web hosting, then expanding into website, e-commerce, email and cloud — the same land-and-expand path GoDaddy runs with its SMB base.

This begins with the entry point of domain and web hosting and then, over time, leads to demand for additional services as the business grows […] the continuous expansion of the website, additional e-commerce solutions, and office and e-mail offerings. Eventually, other cloud-oriented services such as storage, backup, and security services are added.

p. 9 · Read in context →

IONOS's reported customer base of 6.63 million at the end of fiscal 2025, after adding roughly 307,000 net customers during the year.

Overall, the number of customers increased by approximately 307,000 in fiscal year 2025, bringing the total to 6.63 million customers.

p. 19 · Read in context →

IONOS's self-positioning as one of Europe's leading SMB digital-transformation partners, claiming a strong web-hosting and cloud market position across Europe and North America.

As one of Europe's leading digital transformation partners for small and medium-sized businesses, IONOS has established a strong market position in the web hosting and cloud sectors in Europe and North America.

p. 53 · Read in context →

Shopify Inc. (SHOP)

Shopify is the leading commerce platform and the principal rival to GoDaddy's fast-growing Applications & Commerce segment, competing for the same aspiring entrepreneurs building and selling online.

Shopify's stated pace of new-entrepreneur formation — a first sale every 26 seconds — framed by its President as growing the total market rather than taking share, targeting the same aspiring entrepreneurs GoDaddy pursues.

Harley Finkelstein (President): Every 26 seconds, a new entrepreneur makes their first sale on Shopify. […] That is TAM expansion at its best. And any of those merchants could easily become one of the world's biggest brands in a decade or less.

p. 6 · Read in context →

Shopify's reported scale — millions of merchants across more than 175 countries, 44% of them in the United States — the merchant base its commerce platform brings against GoDaddy's.

As of December 31, 2025, we had millions of merchants from more than 175 countries using our platform, geographically dispersed as follows: 44% in the United States, 31% in Europe, the Middle East and Africa, 16% in Asia Pacific, Australia and China, 5% in Canada and 5% in Latin America.

p. 7 · Read in context →

Shopify's description of its multi-channel commerce platform spanning online storefronts, physical retail, social and AI surfaces — the online-store and selling tools that overlap GoDaddy's Applications & Commerce products.

Shopify's business is designed to empower our merchants by offering a comprehensive, multi-channel commerce platform that supports their business as it grows. As owners and operators, merchants set their course, while Shopify offers them the tools to seamlessly manage, market and sell their products across various sales channels, including online storefronts, physical retail spaces, AI platforms, social media and more.

p. 7 · Read in context →

Tucows Inc. (TCX)

Tucows is a direct competitor in GoDaddy's core domains business — a top wholesale and retail registrar and domain-aftermarket operator — offering an outside read on domain-industry volumes and channel structure.

Tucows' reported 21.5 million domains under management across its OpenSRS, Enom, EPAG and Ascio registrars — and a 12.3% year-over-year decline — in a domains market GoDaddy leads.

Together the OpenSRS, Enom, EPAG and Ascio Domain Services manage 21.5 million domain names under the Tucows, Enom, EPAG and Ascio ICANN registrar accreditations and for other registrars under their own accreditations. Domains under management has decreased by 3.0 million, or 12.3%, since December 31, 2024.

p. 7 · Read in context →

Tucows' description of its wholesale distribution model — a network of more than 32,000 resellers in roughly 200 countries — a channel-led approach distinct from GoDaddy's retail-direct domains business.

Our primary distribution channel is a global network of more than 32,000 resellers that operate in approximately 200 countries and who typically provide their customers, the end-users of Internet-based services, with solutions for establishing and maintaining an online presence.

p. 7 · Read in context →

Tucows' self-positioning in the wholesale domain-registration and email markets, citing its registrar brands and its status among the first group of ICANN-accredited registrars in 1999.

We believe that we are well positioned in the wholesale domain registration and email markets due in part to our highly-recognized "Tucows", "OpenSRS", "Ascio" and "Enom" brands and the respect they confer on us as a defender of end-user rights and reseller-friendly approaches to doing business. We were among the first group of 34 registrars to be accredited by ICANN in 1999, and we remain active in Internet governance issues.

p. 8 · Read in context →

GMO Internet Group, Inc. (9449)

GMO Internet is one of the world's largest domain registrars and a major web-hosting provider, competing with GoDaddy's domains and hosting core — and, like GoDaddy, selling a one-stop SMB bundle of domains, servers, commerce and payments.

GMO Internet's stated positioning as Japan's number-one internet infrastructure and security provider, citing 8,000 partners and over 17 million customer subscriptions across its domain, hosting, payment and security businesses.

Masatoshi Kumagai (Founder, Chairman & Group CEO): Now we have 8,000 partners, providing Japan's number one infrastructure and security, and a very large number of customers with over 17 million subscriptions.

p. 13 · Read in context →

GMO's account of its internet-infrastructure segment — with cloud computing and rental servers among the drivers of a tenth consecutive year of record profit — the hosting business that overlaps GoDaddy's.

Masashi Yasuda (Director, EVP & Group CFO): Here are the full-year results of the infrastructure business. On the strength of its revenue model of bedrock stock earnings, the Company achieved its highest performance for the 10th consecutive fiscal years. In FY2025, cloud computing, rental servers, and settlement services, centered on GPU Cloud, performed well.

p. 68 · Read in context →

BigCommerce Holdings, Inc. (BIGC)

BigCommerce is a SaaS commerce platform competing for SMB online stores, though it has pivoted upmarket toward mid-market and enterprise B2B — placing it at the edge of GoDaddy's SMB commerce turf.

BigCommerce's description of its product portfolio — including the Makeswift site builder — and a dedicated Small Business offering group, the SMB-facing commerce and site-building tools that overlap GoDaddy's.

Travis Hess (CEO): We have three owned products in our portfolio today: our flagship commerce platform, BigCommerce, our AI-based product data feed management platform, Feedonomics, and our brand and commerce site builder and visual editor, Makeswift. […] We have integrated all three products both operationally and commercially and have organized the teams around three offering groups, B2C, B2B, and Small Business.

p. 2 · Read in context →

BigCommerce's CEO maps the SMB e-commerce competitive set — naming WooCommerce, Shopify and Magento as the platforms merchants migrate between — the platform market GoDaddy's commerce products also sit in.

Brent Bellm (CEO): I would say at the upper end, Custom and Magento followed by Shopify have been the biggest migrations over time. At the SMB level, it's a wide range. It's WooCommerce, it's Shopify, it's Magento as well.

p. 10 · Read in context →

More peer documents

Wix.com — Q1 FY2026 earnings call — Q1 FY2026 · 26 pages · Wix's push into AI-driven creation — the Base44 AI app-building acquisition and explicit market-share and TAM-expansion goals for web creation. · Open →

Wix.com — FY2023 annual report (Form 20-F) — FY2023 · 324 pages · The prior-year competition section that also names GoDaddy, showing the head-to-head framing is persistent, not a one-off. · Open →

Shopify — Q1 FY2026 earnings call — Q1 FY2026 · 38 pages · Shopify Payments at 67% GMV penetration and Shop Pay growth — the merchant-payments layer that competes with GoDaddy's commerce and payments. · Open →

Shopify — FY2024 annual report — FY2024 · 198 pages · Fuller merchant-base and competition discussion for the year-over-year trendline behind the FY2025 scale figures. · Open →

Tucows — FY2024 annual report (Form 10-K) — FY2024 · 180 pages · Prior-year domains-under-management base (before the FY2025 decline), useful for sizing the domain-industry contraction GoDaddy is navigating. · Open →

GMO Internet Group — FY2025 annual report (Japanese) — FY2025 · 244 pages · Japanese-language segment detail on GMO's infrastructure business — 14.24 million managed domains, ~44,000 hosting contracts, and claimed #1 domestic share in domains, servers, commerce and payments. · Open →

BigCommerce — Q1 FY2025 earnings call — Q1 FY2025 · 15 pages · Quantifies BigCommerce's split — 5,825 enterprise accounts alongside tens of thousands of small-business accounts and ~$351M ARR — showing how much SMB base overlaps GoDaddy. · Open →

Tucows — Q1 FY2026 earnings call — Q1 FY2026 · 3 pages · Latest management commentary on the domains business and aftermarket/expiry-auction dynamics that GoDaddy also competes in. · Open →

GoDaddy: The Business and the Setup

GoDaddy is the world's largest domain-name registrar and a subscription platform for small-business web presence: about 20.4 million customers, roughly 81 million domains under management, and $4.95 billion of revenue in 2025. It has grown free cash flow every year for a decade, to $1.6 billion, and used it to shrink the share count. The stock has since fallen about 58% from its January 2025 high while that cash flow kept rising — the gap that defines the investment question.

What GoDaddy does

GoDaddy sells the plumbing of being online. An entrepreneur registers a domain name, points it at a website, adds email, payments and marketing tools, and pays GoDaddy a recurring subscription for each piece. The company describes itself as a global leader serving entrepreneurs as a "one-stop shop," and reports about 20.4 million customers as of December 31, 2025 [1].

The foundation is domains. GoDaddy is the largest domain registrar in the world, with roughly 81 million domains under management at the end of 2025 — about 21% of the roughly 387 million domains registered worldwide — and approximately 94% of its customers hold a domain bought from GoDaddy [2]. The domain is the entry point; the higher-value products — website building, commerce, payments, email and security — are sold on top of that relationship.

The business reports in two segments. Core Platform ($3.06 billion in 2025) is domains plus hosting and security. Applications & Commerce ($1.89 billion) is the software layer: website builders, GoDaddy Payments, and resold productivity tools such as Microsoft 365 [3]. Within Core, domains alone generated $2.31 billion [4]. Applications & Commerce is the faster-growing, higher-margin end and the segment management is pushing hardest.

Source: FY2025 Annual Report (Form 10-K), segment and disaggregated-revenue disclosures [5] [6].

The revenue is overwhelmingly recurring and paid in advance. Customers typically pay at the time of sale for subscription terms that can run from one month to ten years, and GoDaddy recognizes that cash as revenue ratably over the term. The result is a large customer-funded balance: $3.32 billion of deferred revenue at year-end 2025 — about eight months of revenue booked but not yet recognized [7]. That float is why the business converts profit to cash so heavily, and why a soft quarter is slow to show up in reported revenue.

The scale, in numbers

Customers (millions)

Revenue per Customer ($)

Domains Managed (millions)

Annualized Recurring Revenue ($M)

Source: FY2025 Annual Report (Form 10-K), MD&A Key Performance Indicators [8].

The shape of growth has shifted from adding customers to earning more from each one. The customer count is roughly flat — 20.4 million, down slightly from 21.0 million in 2023 — while average revenue per customer has climbed to $242 and annualized recurring revenue reached $4.34 billion on total bookings of $5.4 billion [9]. Growth now comes from pricing, bundling and attaching commerce and software to an existing base, not from a rising headcount of customers. About two-thirds of revenue is generated in the United States, one-third internationally.

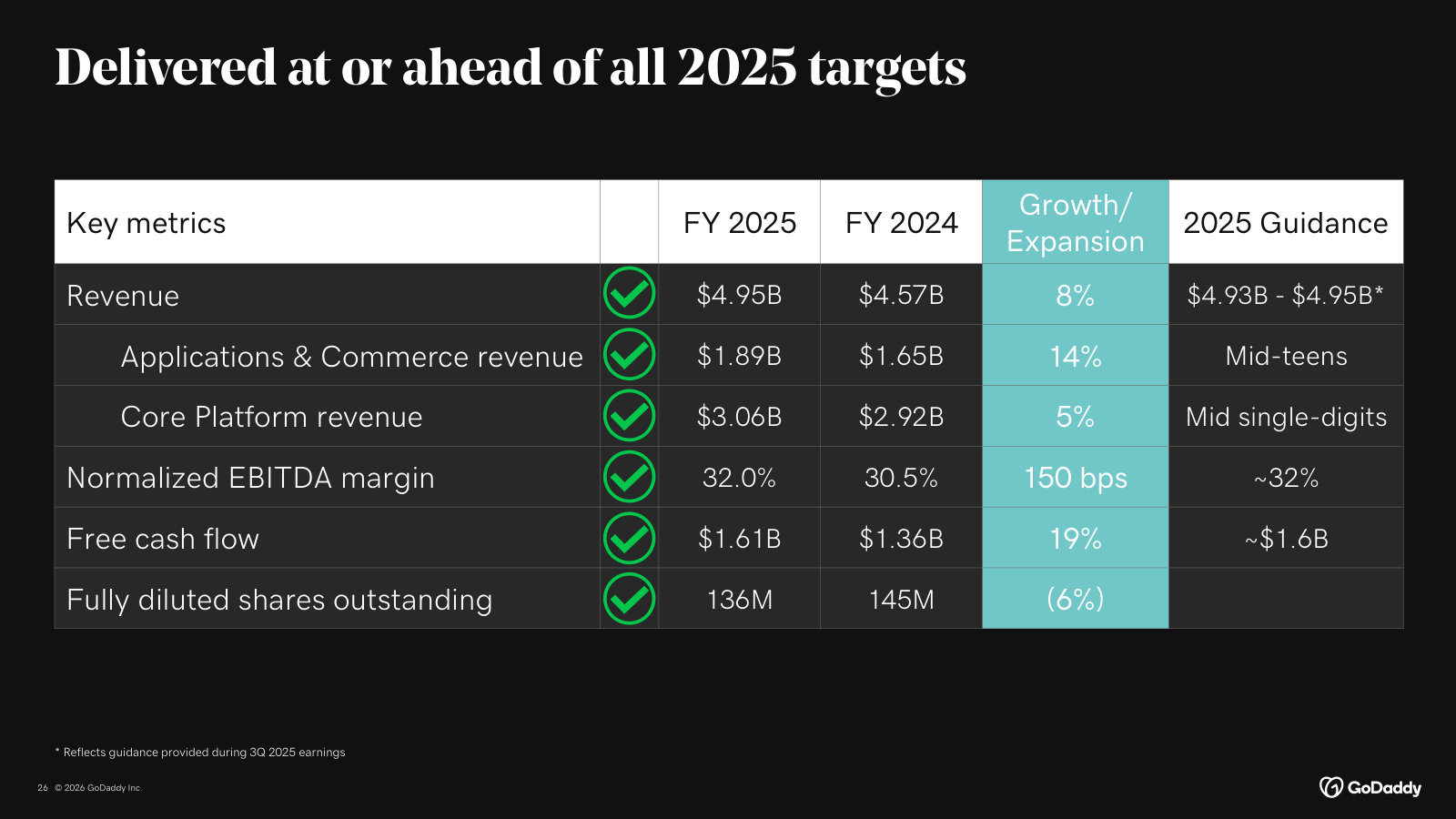

In 2025 that produced revenue of $4.95 billion, up 8.3%, operating income of $1.13 billion (a 22.8% operating margin) and net income of $875 million, or $6.22 in diluted earnings per share [10].

A decade of rising cash flow

The reason this company is worth studying for a cash-flow-focused investor is the record below. Revenue has roughly tripled since 2016, but the more striking series is free cash flow, which has risen in every single year of the decade — through a pandemic, a rate cycle, and a leadership change — from $325 million in 2016 to $1.58 billion in 2025.

Source: derived from reported financials, FY2016–FY2025 (Consolidated Statements of Cash Flows) [11].

Two features stand out. First, the gap between free cash flow and net income runs the "wrong" way for a skeptic's instinct: free cash flow of $1.58 billion in 2025 exceeded net income of $875 million, because the deferred-revenue float and low capital intensity mean cash arrives ahead of accounting profit [12]. Second, capital intensity is minimal: capital expenditure was $23.9 million in 2025, under 0.5% of revenue [13]. This is a business that grows without needing to reinvest much cash.

One honest qualifier belongs here at the outset: reported free cash flow does not charge for stock-based compensation, which was $318 million in 2025 [14]. Deducting it would lower the true owner's cash yield by roughly a fifth. The consistency of the cash flow is real; its exact level deserves the scrutiny a later chapter can give it.

What management does with the cash

Because the business needs so little reinvestment and pays no dividend, nearly all of the cash goes to buying back stock. GoDaddy repurchased $1.6 billion of its shares in 2025 and has bought back roughly $5.4 billion over the past five years [15]. The board's authorization was raised to a cumulative $4.0 billion through 2025 and, in April 2025, extended by a further $3.0 billion through 2027, with $2.17 billion still available at year-end [16].

Source: Consolidated Statements of Cash Flows, FY2021–FY2025 [17].

The buybacks have shrunk the count: Class A shares outstanding fell to 134.7 million at year-end 2025 from 141.2 million a year earlier [18]. There is a fair counter-point on timing, worth flagging early: much of the 2025 repurchasing was done through accelerated programs at a weighted-average price of about $176 per share [19] — roughly double today's price. Buying back stock is only value-accretive at the right price, and 2025's buying was not cheap. Whether the remaining $2.17 billion authorization is deployed better from here is a question for the reader to track.

The setup: a 58% decline against a rising business

Here is the tension that makes GoDaddy a decision rather than a description. The shares peaked near $214 in January 2025 and traded around $89 in July 2026 — a decline of roughly 58%. Over the same stretch, revenue accelerated to 8.3% growth and free cash flow set a fresh record [20]. The price re-rated; the cash flows, so far, did not.

Source: market price data, monthly closes January 2024–July 2026 (as reported).

At about $89 on roughly 140.6 million diluted shares, GoDaddy is valued near $12.5 billion of equity, or about $15.2 billion of enterprise value after $2.7 billion of net debt. Against $1.58 billion of reported free cash flow, that is a free-cash-flow yield of roughly 12.6% on the equity — closer to 10% measured against enterprise value, and lower again once stock-based compensation is charged.

Share Price ($)

Equity Value ($B)

FCF Yield (on equity)

Net Debt ($B)

Source: derived from market price data (July 2026) and FY2025 Annual Report balance sheet and cash-flow statement [21] [22].

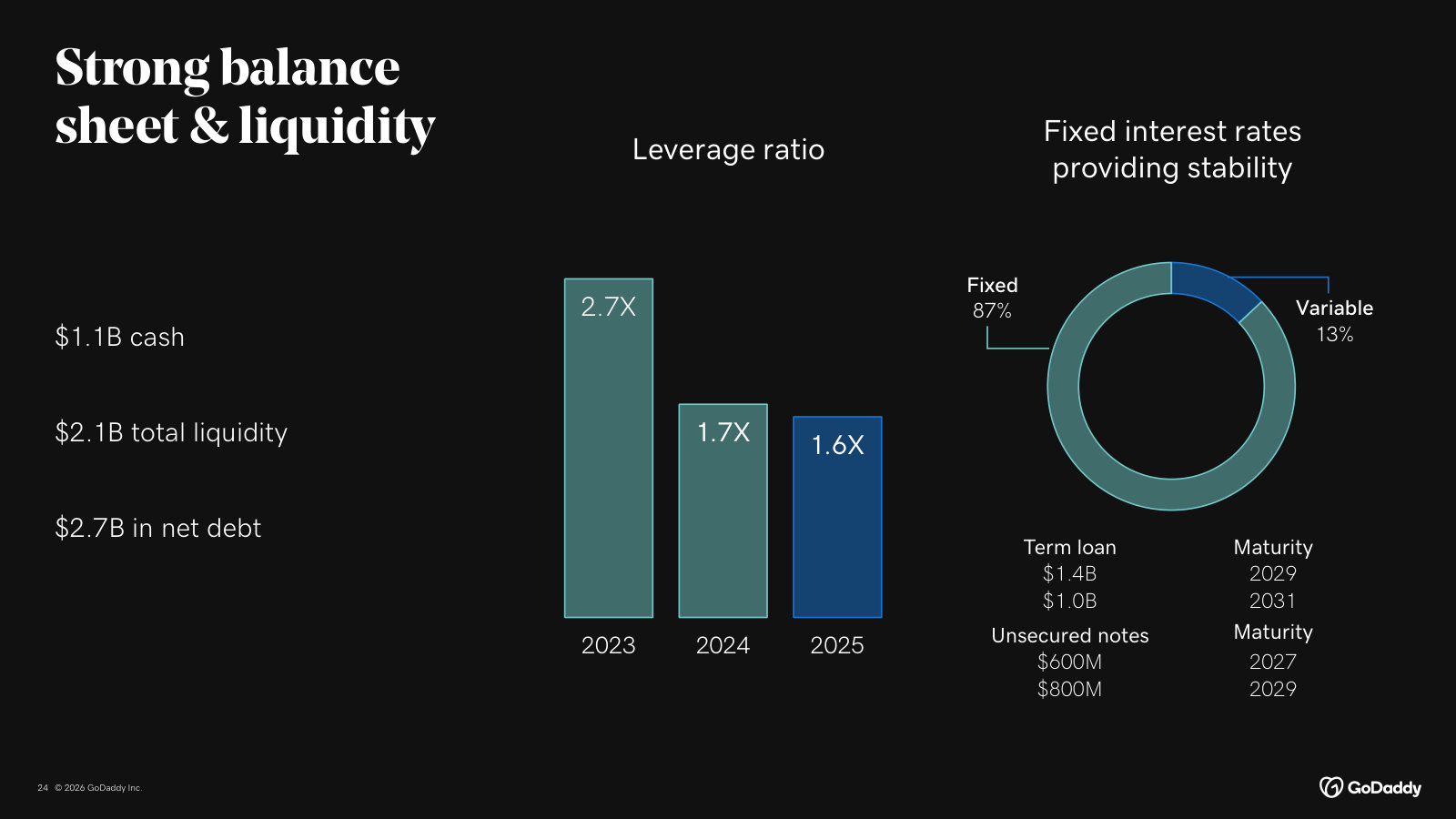

The balance sheet carries $3.78 billion of debt against $1.08 billion of cash, so net debt is about $2.7 billion — roughly 1.7 times a single year of free cash flow [23]. That is modest leverage for a business this cash-generative, though not the net-cash position a conservative screen prefers. The $3.32 billion of deferred revenue is a customer-funded obligation to deliver service, not borrowed money, and the company does not count it as debt — a distinction that matters to how the balance sheet is read, and one a later chapter should test directly.

The question this report exists to answer

The pieces above frame a single analytical question, and it is the spine of everything that follows:

Can GoDaddy's domain-and-web-presence franchise keep compounding the roughly $1.6 billion of free cash flow it now produces — so that a decade out that cash flow is reliably higher, not lower — and is that durability being priced, after a 58% decline, at a double-digit free-cash-flow yield?

Both halves are contestable. The bull case is a near-monopoly registrar with a customer-funded float, a decade of unbroken cash growth, and a price that has halved while the fundamentals improved — the kind of gap between market value and cash-flow value that rewards patience. The bear case is that the same halving reflects a real threat: artificial-intelligence tools that let anyone spin up a website and a name in seconds may erode the very attach-and-upsell engine that lifts revenue per customer, and management's own filings now frame the company's future around an "agentic" internet it is racing to stay ahead of [24]. Whether the moat is durable enough to make year-ten cash flow a safe bet, and whether the current price pays for that durability with margin to spare, is what the rest of this report sets out to weigh.

Cash Quality

GoDaddy's $1.58 billion of free cash flow is real cash, not an accounting artifact: it arrives ahead of accounting profit, capital spending is negligible, and there are no working-capital tricks propping it up. Two honest charges change the picture, though. Stock compensation is a genuine cost the headline number ignores, and the company is paying almost no cash tax because of a shield that is running down. Charge both and the owner-cash yield falls from roughly 12.6% toward 7% to 8.5%. The balance sheet holds no tangible equity; the asset is the recurring cash, not the assets on the page.

Free Cash Flow FY2025 ($M)

Cash Tax Rate FY2025

Stock Comp FY2025 ($M)

Tangible Common Equity ($M)

Sources: FY2025 10-K, Consolidated Statements of Cash Flows [1]; Consolidated Balance Sheets [2]; Cash Taxes disclosure [3].

From profit to cash

The starting point is that GoDaddy's cash generation is more stable than its reported profit. Net income has swung from a $495 million loss (FY2020) to $1.37 billion (FY2023) and back to $875 million (FY2025); operating cash flow, over the same span, rose in a straight line from $765 million to $1.60 billion [4]. For a subscription business collected in advance, cash is the cleaner signal, and it is the signal the investment case in Domains and Cash Flow rests on.

Source: FY2025 10-K, Consolidated Statements of Cash Flows (FY2023–25) and reported financials (FY2020–22) [5].

The one year net income sat above free cash flow — FY2023 — is the exception that proves the rule. That year's profit was lifted by a $993.2 million non-cash deferred-tax benefit, booked when GoDaddy released most of the valuation allowance on its U.S. deferred tax assets [6] [7]. Strip that one entry out and the decade of cash generation is monotonic while reported earnings are not. The gap between the two is explained by three recurring items — depreciation and amortization, stock compensation, and the deferred-revenue float — and by the tax line.

The two charges a skeptic makes

Reported free cash flow adds back $317.8 million of stock-based compensation and does not treat it as a cost [8]. That is a real economic charge — equity handed to employees is value transferred from shareholders — running at about 6.4% of revenue. GoDaddy has more than offset the dilution with buybacks (Class A shares fell from 141.2 million to 134.7 million in FY2025) [9], but the buybacks cost cash the free-cash-flow line already counts as available. Charging stock comp is the first adjustment.

The second is tax. GoDaddy paid $16.5 million of cash income tax in FY2025 on $1,020.0 million of pretax income — an effective cash rate near 1.6%, against a book tax expense of $145.0 million and a 21% federal statutory rate that would imply roughly $214 million [10] [11]. Cash tax has been trivial for years — $10.6 million (FY2023) and $19.1 million (FY2024) [12]. That is a benefit, not a permanent feature.

Sources: FY2025 10-K, Cash Taxes disclosure [13]; statutory figures derived from pretax income, Consolidated Statements of Operations [14].

The shield behind the low cash tax is a net deferred tax asset of $1,047.9 million, dominated by $571.2 million of net operating losses and $243.0 million of tax credits, and it is depleting: it fell $113.4 million in FY2025 alone [15]. Gross federal net operating losses of $2,429.7 million remain [16], so cash taxes stay suppressed for several more years, but as the carryforwards are used up cash tax normalizes toward book — an eventual drag on free cash flow of roughly $150 million to $200 million a year at current profit levels.

Putting both charges through the arithmetic reframes the yield. Against the roughly $12.5 billion equity value and $15.2 billion enterprise value established in Domains and Cash Flow, the headline free cash flow is a 12.6% equity yield. Charge stock comp and it is about 10.1%; normalize cash tax as well and it is about 8.5% on equity, near 7.0% on enterprise value.

Source: derived from FY2025 reported cash flow, stock compensation, and cash-tax disclosures; yields against the equity and enterprise value in Domains and Cash Flow [17].

Source: derived from reported financials, FY2025 10-K [18]; the normalized-tax line is illustrative, applying a ~20% cash rate to pretax income.

Even fully burdened for stock compensation and a normalized tax rate, GoDaddy still throws off roughly 7% to 8.5% of its market value in owner cash each year. The point is calibration, not alarm: the headline 12.6% yield flatters the sustainable figure by about 400 basis points, and the tax half of that gap is a matter of when, not if.

The float, and a balance sheet with no equity

What a skeptic will not find is manufactured cash. GoDaddy collects subscriptions in advance, so it carries $3,319.1 million of deferred revenue — $2,384.2 million current and $934.9 million longer-dated — which is customer money held before the service is delivered [19] [20]. That float grew by $206.8 million in FY2025 and contributed to operating cash flow [21] — a real tailwind, but a contained one at about 13% of the year's operating cash; the bulk of the cash is generated by the business, not by the float expanding. The float is a debt of service, not of money: it is discharged by delivering hosting and domains at near-zero marginal cost, which is why the company does not — and should not — count it as debt in its net-debt math.

The rest of the working capital is clean. Receivables are $83.1 million against $4.95 billion of revenue — roughly six days of sales, and lower than a year earlier — because customers pay up front; there is no inventory to age [22]. Accounts payable actually fell, from $148.1 million (FY2023) to $67.5 million, and were a use of cash in the year, not a source [23] [24]. Stretching suppliers to flatter cash flow is a common late-cycle tell; the opposite is happening here.

The balance sheet itself will not anchor a valuation. Total stockholders' equity is $215.1 million, but that sits on top of $3,633.3 million of goodwill and $986.3 million of other intangibles, leaving tangible common equity of roughly negative $4.4 billion, and an accumulated deficit of $2,789.4 million after a decade of buybacks and past losses [25] [26]. Price-to-book is not a meaningful lens for this company; what is being bought is a recurring-cash annuity, and the earlier chapters price it as one.

Net debt sits at about $2.70 billion — total borrowings of $3,780.3 million less $1,080.9 million of cash — or roughly 1.7 times free cash flow, and closer to 2.1 times once cash flow is charged for stock comp [27]. The maturities are termed out and laddered, with the nearest wall a $600 million note due December 2027, then term loans and notes falling in 2029 and 2031 [28]. Cash interest ran $139.5 million, under 9% of operating cash flow [29]. No single year's cash flow is at the mercy of a refinancing.

Source: FY2025 10-K, Note 9 Long-Term Debt [30].

What would change the read

The evidence points to genuine cash quality: operating cash flow has risen every year for a decade, capital intensity is negligible, the deferred-revenue float is a structural feature rather than a trick, and the working capital shows no signs of being managed for appearances. The strongest fact against the bullish reading is not fraud but flattery — the headline yield overstates sustainable owner cash because it ignores a real 6.4%-of-revenue stock-comp charge and rests on a cash-tax rate that is temporary. What would change the read in either direction is observable: cash taxes climbing toward the high-teens as the carryforwards deplete, or stock comp staying near current levels, would pull the sustainable yield toward 7%; a durable float and continued sub-1%-of-revenue capital spending would hold it nearer the top of the 7%-to-8.5% band. The number to watch is cash tax paid, disclosed each year in the tax note.

Moat and Durability

GoDaddy clears a real moat bar: a customer retention rate of about 85% held for five straight years, roughly 90% for customers past their third year, more than 89% of revenue coming from customers who were already customers a year earlier, and 21% of the world's registered domains under one roof [1] [2]. But the engine underneath has quietly changed. Since 2023 revenue rose about 16% while the customer count and the domain base each shrank about 3% — the growth is entirely higher spend per customer, not more customers [3]. Whether year-ten cash flow is higher now depends on how far that per-customer figure can travel in an internet being reshaped by AI.

The moat, measured

A moat that matters shows up in retention, and GoDaddy's does. Its blended customer retention rate has sat at roughly 85% in each of the five years through 2025 (about 84% in 2024, held down by deliberate divestitures and product end-of-life), and it climbs to roughly 90% once a customer is past three years with the company. More than 89% of 2025 revenue came from prior-year customers [4].

The single most telling disclosure is the cohort math. GoDaddy acquired about 5.0 million customers in 2017 for $253.2 million of marketing spend; by the end of 2025 that one cohort had generated roughly $3.0 billion of cumulative bookings, at an average annual revenue retention rate above 91% over the seven years [5]. A cohort that returns roughly twelve times its acquisition cost over eight years, while spending more each year, is the definition of a low-churn subscription franchise with real switching costs.

Retention Rate

Retention, 3+ Year Customers

Revenue From Prior-Year Customers

Share of World Domains

Source: FY2025 Annual Report (Form 10-K), MD&A and Item 1 Business [6] [7]; "over 89%" and "approximately 90%" shown at their disclosed thresholds.

The switching cost is concrete rather than contractual. A customer who leaves does not just cancel a subscription; they move the domain that is their address on the internet, the email tied to it, the website built on GoDaddy's tools, and increasingly the payments and commerce plumbing behind it. About 94% of GoDaddy customers hold a domain with the company, and the domain is the anchor the rest attaches to [8]. Scale reinforces it: roughly 81 million domains under management, about 21% of the roughly 387 million registered worldwide, the largest single position in the industry [9].

Where the growth actually comes from

The moat holds the base. It is not adding to it. Total customers slipped from 21.0 million at the end of 2023 to 20.4 million at the end of 2025, and domains under management fell from 83.6 million to 80.8 million over the same span [10]. What rose was average revenue per user — from $203 to $242, up about 19% in two years, and up from $170 in 2020 [11]. Revenue growth is a pricing-and-mix story on a flat-to-shrinking unit base, not a customer-acquisition story.

Source: derived from reported operating metrics, FY2025 Annual Report (Form 10-K); revenue, ARPU, total customers and domains under management indexed to FY2020 [12].

Two forces drive the rising ARPU, and both are healthier than a simple price hike. The first is bundling and list-price increases across the domain and presence products — domains revenue rose 7.3% in 2025, from $2,152.7 million to $2,310.5 million, even as the domain count edged lower, which is close to pure price [13]. The second is mix: the higher-margin Applications & Commerce segment (email, websites, payments, commerce software) grew from $1,430 million of revenue in 2023 to $1,889 million in 2025, a 32% two-year gain against 8% for Core Platform, and it carries the richer segment margin [14]. Customers are buying more products, not just paying more for the same one — and the company's own data shows multi-product customers retain at higher rates [15].

Source: FY2025 Annual Report (Form 10-K), Results of Operations [16].

This is where the durability question sharpens. Raising ARPU roughly 8–10% a year on a stable base is a fine model for years, and higher lifetime spend on loyal multi-product customers is exactly what a compounder wants. But it is a narrower base to grow from than a rising customer count, and it leans on continued pricing power and attach — the very levers most exposed if the reason a customer needed GoDaddy in the first place gets easier to satisfy elsewhere.

The competitive set and the disintermediation risk

The near-in competition is fragmented and, on the evidence, contained. GoDaddy names a long roster across its markets — Newfold Digital, Namecheap, Tucows, GMO, Cloudflare and Identity Digital in domains and hosting; Wix, Squarespace, Automattic, IONOS and the hyperscalers Google, Amazon and Microsoft across presence and commerce — and describes the market as "highly fragmented and competitive" [17]. No single rival is taking the domain franchise; 21% global share has been stable, and retention has not cracked under a decade of this competition. Fragmentation, held off by scale and switching costs, is a manageable condition, not the threat that halved the stock.

The threat that matters is stated plainly in GoDaddy's own risk factors. "The widespread acceptance of any alternative system, such as mobile applications, AI-powered products and tools or closed networks, could eliminate the need to register a domain name or to establish an online presence," and as reliance on social channels and AI tools grows, "domain names, websites and online stores and marketplaces may become less prominent, and their value may decline" [18]. The company adds that it expects "more competition… from both traditional and non-traditional competitors" as products fill with AI and large language models [19]. This is the bear thesis: if an entrepreneur can stand up a presence by describing it to an AI agent — with no domain to register and no website to build — the attach-and-upsell funnel that lifts ARPU loses its starting point.

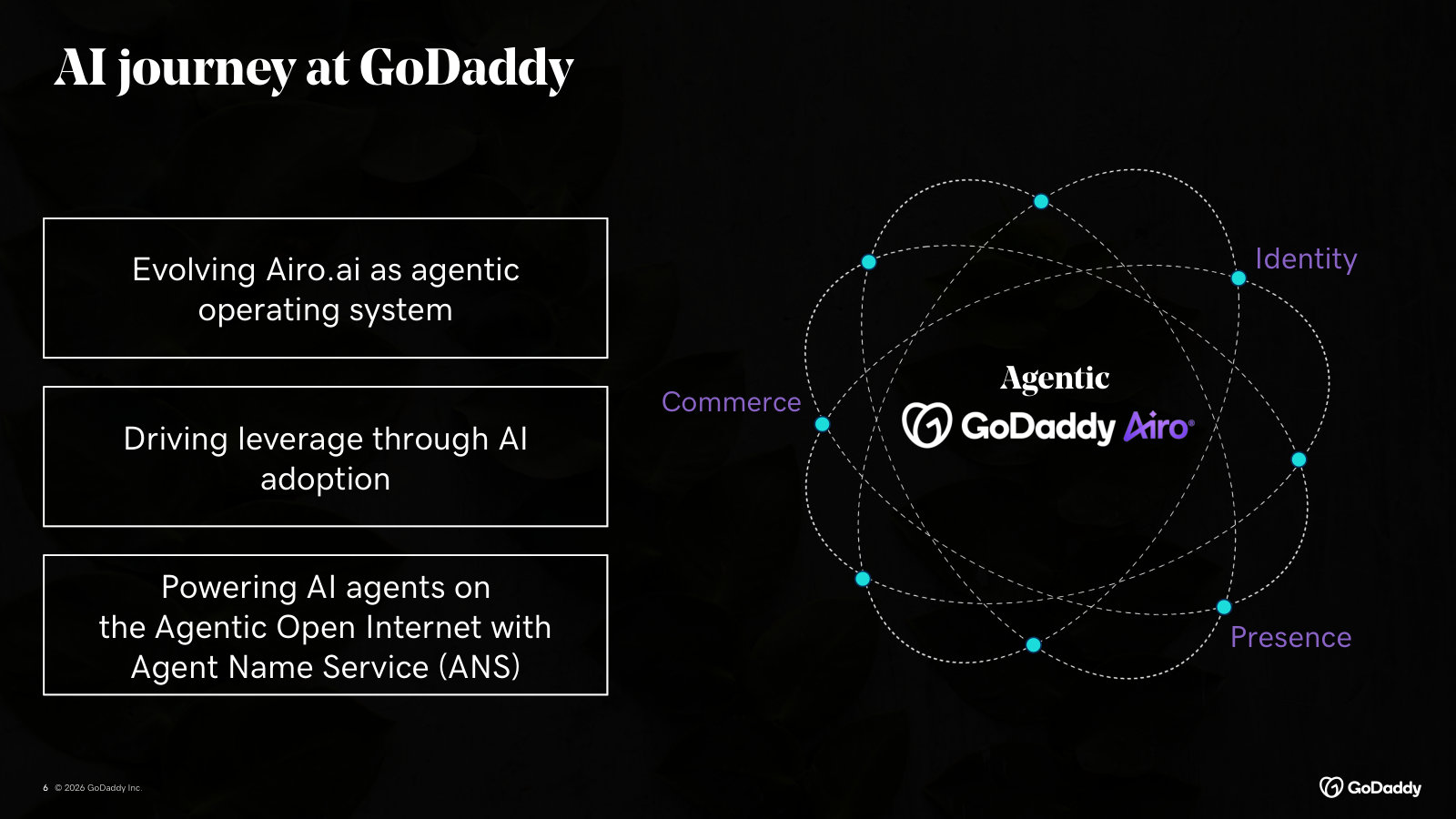

Management's answer: Airo and ANS

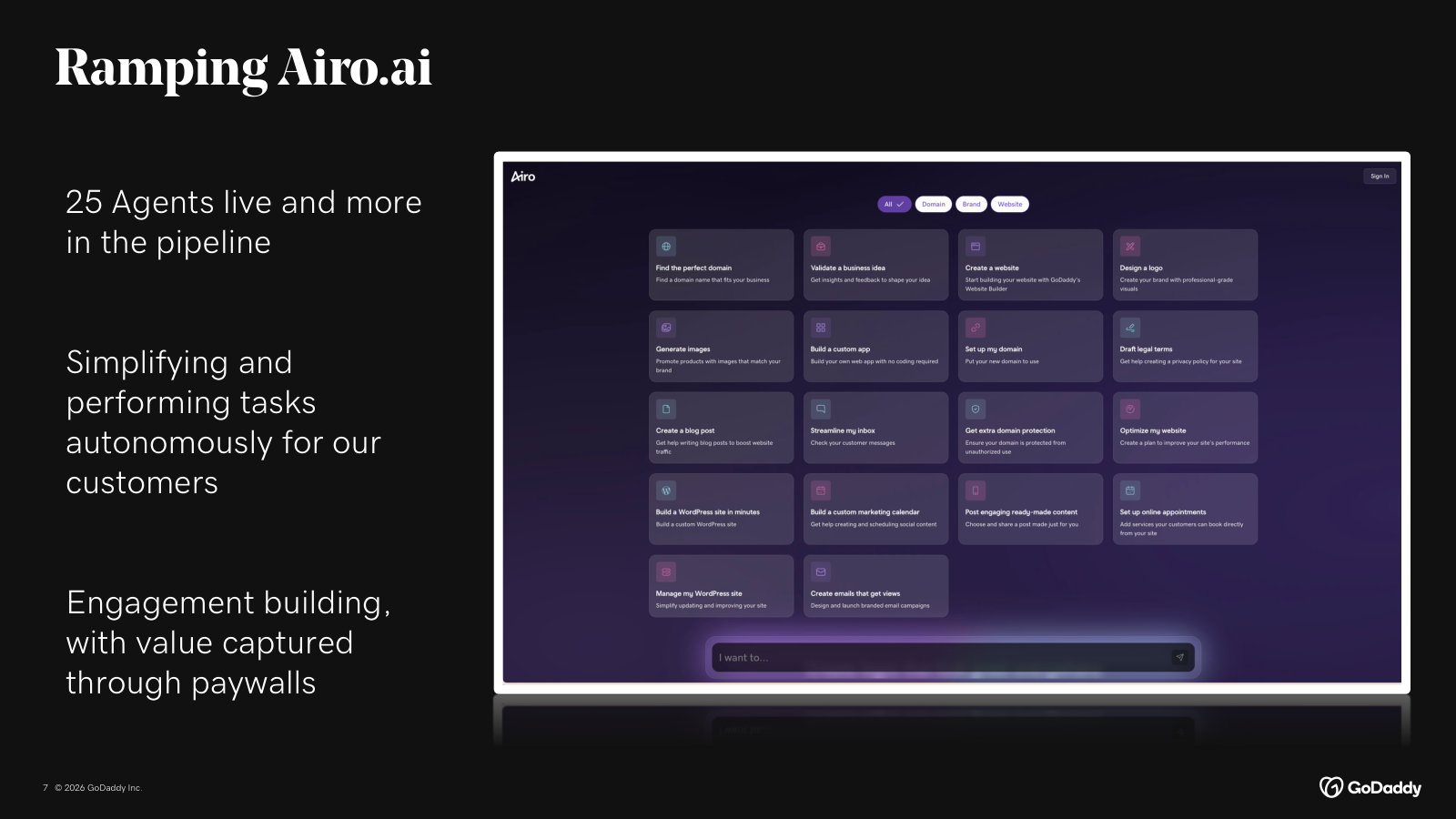

GoDaddy is not standing still, and it is worth weighing what it has built rather than dismissing it. Two responses stand out.

The first is monetizing AI inside its own funnel. GoDaddy Airo, its AI experience spanning domains, sites, logos, email and marketing, has moved from a generative toolset toward an agentic one, and the company has begun charging for it — Airo Plus is positioned as a direct monetization vehicle, with paywalls inside the experience [20]. This turns the AI shift from pure threat into a potential new price lever on the same base.

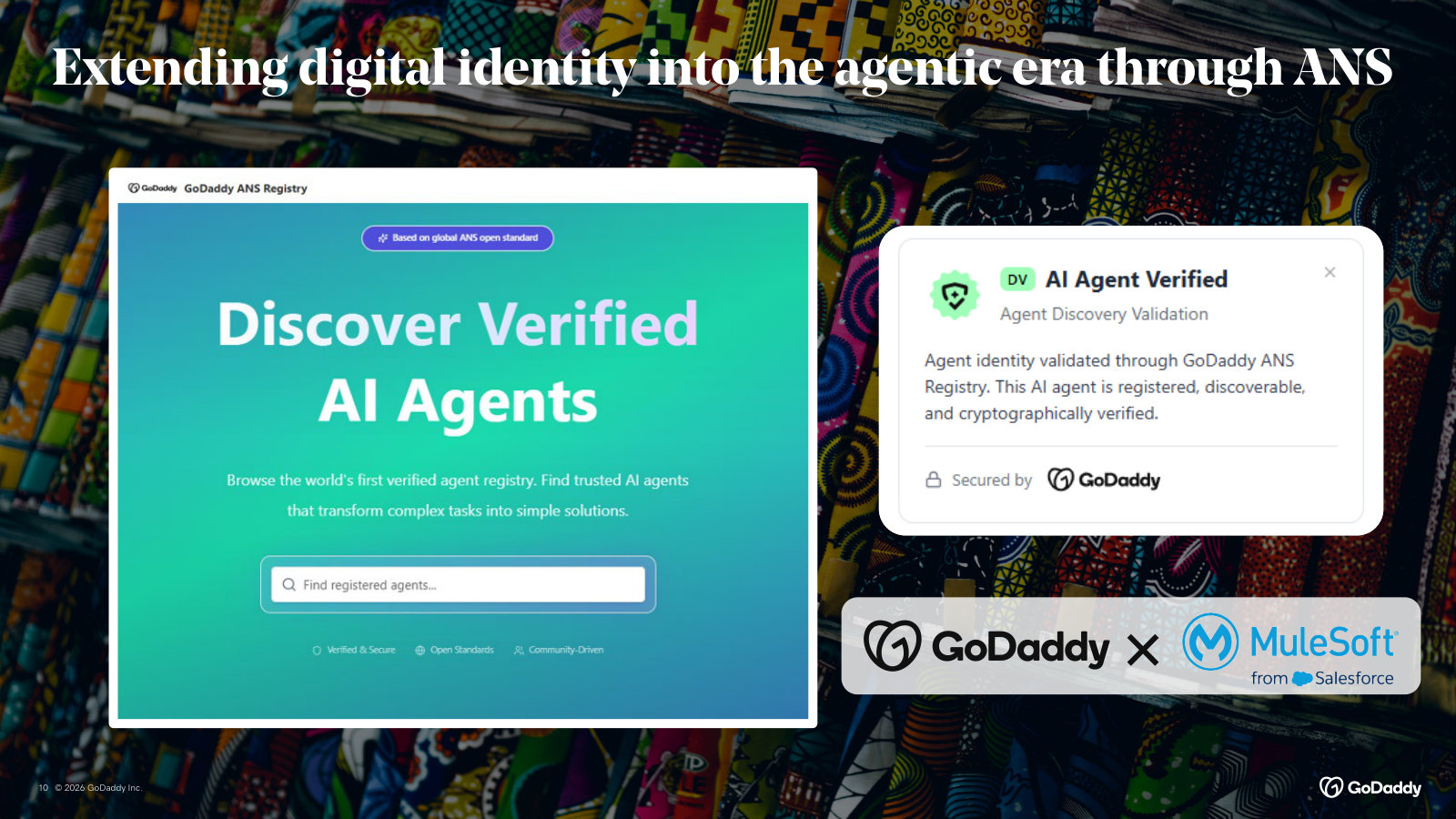

The second is more strategically interesting. GoDaddy has launched Agent Name Service (ANS), an open architecture that anchors AI-agent identity to the domain name system — the same DNS infrastructure its domain leadership already sits on. ANS is in production, with registered agents operational since the end of 2025, an open API for developers, and a public transparency log [21]. The logic is to convert the disintermediation risk into an extension: if AI agents need discoverable, verifiable identities to transact with one another, and that identity is anchored to domains, then a world of billions of agents could need more domain-based identity, not less. On the Q4 2025 call, management framed its edge as more than 20 million customers, decades of proprietary behavioral data, and distribution at the top of the funnel — the assets it would use to deploy agentic capabilities at scale [22].